Introduction

Month-end money pressure becomes stressful when urgent expenses arrive before salary. Imagine a situation where your car breaks down unexpectedly a week before payday, or an urgent medical test requires a sudden cash outlay. For many beginners and salaried workers, these situations cause intense anxiety. The immediate reaction is often to find the fastest way to get short-term cash, regardless of the terms.

With modern financial technology, getting a micro-loan takes only a few taps on a smartphone. However, beginners often feel confused by the overwhelming number of lending apps, peer-to-peer options, and traditional bank facilities. Because small cash amounts look manageable, it is easy to overlook the high annual interest rates, processing fees, and aggressive repayment timelines attached to them. A poor understanding of these terms can cause severe financial mistakes, turning a small, temporary problem into a compounding cycle of debt.

This blog explains exactly how to navigate the world of micro-borrowing safely. It is written for salaried employees, freelancers, and small business owners who want to understand how to borrow small cash responsibly without compromising their long-term financial health. Relying on structured, real-world finance rules is far better than making rushed emotional decisions under stress. By reading this guide, you will gain a clear roadmap for managing emergency short-term liquidity with absolute transparency and confidence.

Understanding Small Cash Borrowing in Simple Words

Small cash borrowing refers to taking out micro-loans—typically small amounts used to cover brief, unexpected financial gaps. Unlike a long-term home loan or an auto loan, these products are designed to be borrowed quickly and paid back within a short window, often ranging from a few weeks to a few months.

How It Works in Real Life

Lenders evaluate your immediate capacity to repay, often using modern digital underwriting tools rather than requiring extensive asset documentation. They disburse the money directly to your account, but in exchange for this speed and convenience, they charge interest rates and processing fees that are proportionally higher than long-term loans.

Real-World Integration

In everyday life, micro-borrowing bridges the gap between your immediate financial obligations and your next regular cash inflow. It connects directly with personal budgeting and credit health. When used correctly, it functions as an emergency utility tool.

- Beginner-Friendly Example: Suppose you need 5,000 INR for an urgent appliance repair. Borrowing this amount from a regulated micro-lender and paying it back in full on your next salary date is a functional application of short-term credit.

- Common Misunderstanding: Many people assume that because a loan amount is small, its impact on their credit profile is also negligible. In reality, defaulting on a small 2,000 INR loan damages your credit history just as severely as missing a payment on a much larger loan product.

- Practical Takeaway: Small cash credit is a high-cost tool meant exclusively for genuine liquidity emergencies—it is not an extension of your regular disposable income.

Why Borrowing Small Cash Responsibly Is Important

The way you handle minor loans directly impacts your broader financial baseline. Micro-borrowing can affect multiple components of your financial life:

- Savings Protection: Borrowing a structured small amount can sometimes prevent you from breaking long-term fixed deposits or selling off investment assets prematurely during a market dip.

- Credit Score Development: Consistently repaying micro-loans on time builds a positive history of debt management, proving to major credit bureaus that you are a dependable borrower.

- Risk and Emotional Balance: Knowing how to evaluate terms objectively stops you from making panic-driven decisions, reducing the risk of falling prey to predatory, unregulated lending schemes.

- Long-Term Financial Discipline: Learning to calculate the real cost of micro-credit instills a habit of analyzing every financial agreement before signing, paving the way for better budgeting and investment choices down the road.

Practical Scenario

Consider two individuals facing a sudden 10,000 INR medical expense. Individual A panics, downloads the first unregulated app they find, and accepts a loan with a 15% weekly fee. Individual B checks their credit portal, opts for an overdraft from their regular salary bank at a documented annual rate, and settles the balance over two months. Individual B resolves the crisis smoothly, while Individual A faces mounting collections calls and skyrocketing debt within a month.

The Real Problem Readers Face With Micro-Loans

The primary reason borrowers face severe issues with micro-loans is not the concept of borrowing itself, but a systemic gap in financial awareness.

[Financial Stress] ➔ [Rushed Digital Application] ➔ [Overlooked Fees] ➔ [Repayment Shock]

The Information Trap

The internet is flooded with conflicting financial advice, aggressive promotional ads promising “instant zero-interest approvals,” and misleading social media clips. This makes it incredibly difficult for a beginner to filter out safe, regulated options from predatory debt traps.

Behavioral and Structural Pitfalls

- Emotional Stress: When an urgent bill arrives, stress can cloud your judgment, leading you to accept the first available source of cash without reviewing the structural terms.

- Skipping the Fine Print: Many digital applications present lengthy Terms and Conditions in tiny fonts on mobile screens. Borrowers frequently click “Agree” without looking at processing fees, prepayment penalties, or late-repayment schedules.

- Absence of Comparison: Out of convenience or urgency, borrowers often default to the first app they see, completely missing lower-cost alternatives like bank overdraft lines or salary advances.

- Over-reliance on Micro-Credit: It is easy to view these accessible loan apps as a structural solution for chronic month-end deficits, rather than fixing the underlying budgeting issues.

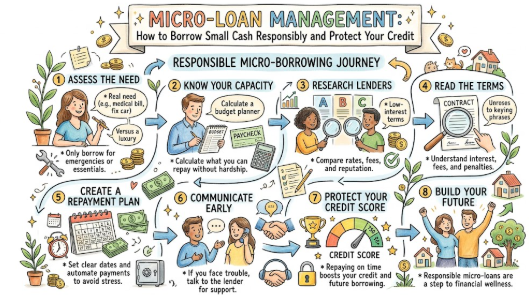

How to Borrow Small Cash Responsibly Step by Step

To ensure small cash loans remain a safe financial tool, follow this clear, step-by-step framework.

Step 1: Validate the Emergency

- What it means: Confirming if the expense requires immediate cash or if it can wait until payday.

- Why it matters: It prevents unnecessary high-cost debt for lifestyle purchases.

- How to apply it: Ask yourself if postponing this payment creates a physical safety hazard or a financial penalty.

- Practical Example: Repairing a leaking pipe is a valid emergency; buying a discounted electronic gadget is not.

- Common Mistake: Treating a limited-time online sale as a financial emergency.

- Better Approach: Set up a separate digital piggy bank for shopping wants and use borrowing strictly for non-negotiable disruptions.

Step 2: Audit Your True Repayment Capacity

- What it means: Calculating exactly how much cash you can spare from your upcoming paycheck to clear the loan.

- Why it matters: It ensures you do not take out a loan you cannot afford to repay on time.

- How to apply it: Review your fixed monthly obligations (rent, utility bills, groceries) and see what is left over to pay down debt.

- Practical Example: If your monthly salary is 40,000 INR and your fixed expenses are 35,000 INR, your absolute maximum capacity to repay a loan next month is 5,000 INR.

- Common Mistake: Assuming your entire salary can go toward clearing a debt, forgetting regular living costs.

- Better Approach: Keep a simple written record of your mandatory monthly costs so you always know your true free cash flow.

Step 3: Check Lender Regulation Status

- What it means: Verifying that the lender is registered with and authorized by national financial regulators (like the RBI in India).

- Why it matters: It protects your personal data from extortion networks and scam apps.

- How to apply it: Look for the lender’s corporate registration number and cross-verify their partner banks on official regulatory websites.

- Practical Example: Checking the “About Us” section of a fintech app to ensure they clearly list their partner Non-Banking Financial Company (NBFC).

- Common Mistake: Installing an unlisted application from an untrusted web link because the ad promised immediate approval.

- Better Approach: Only use institutional portals or apps listed on official national application marketplaces that explicitly state their regulated credentials.

Step 4: Calculate the Annual Percentage Rate (APR)

- What it means: Finding the real total cost of the loan by combining the nominal interest rate with upfront fees.

- Why it matters: Monthly or daily interest rates can hide how expensive a loan actually is.

- How to apply it: Use an online APR calculator to factor in processing fees, documentation costs, and the nominal interest rate over your specific loan period.

- Practical Example: A 1,000 INR loan with a 50 INR fee for 15 days carries a massive annual rate, even though the fee sounds small.

- Common Mistake: Looking only at the base interest rate and ignoring the high upfront processing fees.

- Better Approach: Ask the lender to state the absolute total repayment amount in writing before accepting the cash.

Step 5: Read the Late-Payment and Default Terms

- What it means: Reading the exact penalties, compounding interest adjustments, and collections procedures triggered if you miss a deadline.

- Why it matters: Late fees on small cash products can quickly spiral out of control, eclipsing the original amount borrowed.

- How to apply it: Search the digital loan documentation specifically for terms like “overdue penalty,” “grace period,” or “daily default charges.”

- Practical Example: Knowing that missing your payment date by 48 hours will trigger a flat 500 INR late fee plus additional daily compound interest.

- Common Mistake: Assuming the lender will simply extend your deadline for free if you explain your situation later.

- Better Approach: Establish your repayment plan with a target date 3 days before the official deadline to protect against unexpected banking system delays.

Step 6: Automate the Repayment Process

- What it means: Setting up a standing electronic instruction with your bank to automatically clear the balance on your pay date.

- Why it matters: It removes human error and forgetfulness, protecting your credit score from accidental damage.

- How to apply it: Link your verified primary bank account via a secure national electronic clearing portal (like NACH or e-mandate lines) during the final setup steps.

- Practical Example: Configuring an auto-debit rule scheduled for the morning of the 1st of the month, immediately following your scheduled payroll deposit.

- Common Mistake: Relying on manual calendar reminders, which can easily be missed during a busy work week.

- Better Approach: Set the automated transfer to pull funds from your account the exact same day your salary lands, before you spend money on anything else.

Key Factors That Influence Small Cash Borrowing

When navigating small cash loan platforms, pay close attention to these specific operational variables:

- Interest Calculation Models: Understand whether the interest applies to the reducing balance or functions as a flat percentage on the initial principal. Flat rates look smaller but cost more over time.

- Upfront Processing and Documentation Fees: Lenders often deduct these administration fees directly from the cash they send you. This means you might receive less money than you actually applied for.

- The Credit Score Loop: Your current credit score determines your interest rate options. At the same time, your performance on this loan will immediately update your credit file, impacting your future borrowing power.

- Total Tenure Framework: Shorter terms mean higher individual payments but lower overall interest costs. Longer terms reduce your immediate payment size but increase the total interest paid over the life of the loan.

- Prepayment Rules: Check if the lender charges an extra fee if you want to pay off your balance early once you have the cash. Look for options that offer free prepayment.

Detailed Breakdown of Small Cash Loans

When Borrowing Small Cash Makes Sense

Micro-borrowing is a practical choice when you face a clear, unexpected cost that cannot be delayed without causing major disruption or higher fees.

- Immediate Infrastructure Breakdowns: This includes unexpected repairs for tools or vehicles required for your daily commute or business operations.

- Unplanned Medical Disruptions: Essential prescription purchases or diagnostic tests required before your health insurance processing settles.

- Avoiding Late Penalties: Paying an urgent utility bill to keep your services active when the late fee would cost more than the micro-loan interest.

When Borrowing Must Be Avoided

- Non-Essential Lifestyle Expenses: This includes funding weekend entertainment, buying designer apparel, or upgrading electronics purely for leisure.

- Speculative Investments: Using short-term credit lines to fund stock market trading, cryptocurrency purchases, or betting accounts.

- Clearing Old Loans: Taking out new micro-credit to pay off old debts creates a dangerous, compounding spiral of debt.

Strategic Comparison: Traditional vs. Modern Digital Micro-Credit

Traditional options like salary advances from an employer or structured bank overdrafts usually offer lower interest rates and clearer regulatory guardrails. However, they often require manual paperwork and take longer to approve.

Modern digital credit apps offer instant processing and 24/7 access directly on your phone, but they balance this convenience with significantly higher interest rates, steep processing fees, and shorter repayment timelines.

Common Mistakes Beginners Make With Micro-Loans

Understanding common borrowing mistakes helps you recognize and avoid high-risk lending scenarios.

- Chasing “Zero-Cost” Marketing Claims: Lenders often run ads promising “0% interest interest-free loans.” While the interest rate might be zero, they frequently make up for it with high, non-refundable structural processing fees or account maintenance charges.

- Ignoring the Total Cost of Credit: Borrowers often focus solely on the daily payment amount (e.g., “Only 30 INR a day!”) while ignoring the cumulative cost over the entire term.

- Granting Broad Smartphone App Permissions: Many predatory lending apps require access to your entire contact list, gallery, and location data before processing a loan. This data can later be used for aggressive collection tactics.

- Borrowing from Multiple Platforms Simultaneously: Taking out small loans from several apps at the same time fragments your attention and can quickly overwhelm your monthly budget.

“Don’t Do This” Checklist

- Do not borrow money based on a random text message link or social media ad.

- Do not authorize app permissions that give access to your personal contacts or photos.

- Do not take out a new loan to cover a payment on an existing debt line.

- Do not sign a loan agreement if the lender refuses to give you an explicit repayment schedule.

- Do not skip checking the lender’s regulatory status on the official corporate registry portal.

Practical Real-Life Examples of Small Cash Borrowing

Example 1: Salaried Professional Managing Auto Breakdown

- Situation: A marketing executive needs 8,000 INR for immediate car repairs five days before payday.

- Mistake: Rushing into an unregulated app that demands full access to their phone’s contact list.

- Better Action: Requesting a 10,000 INR short-term overdraft line through their registered payroll bank.

- Learning: Using institutional banking channels keeps your data secure and offers fair, regulated terms.

Example 2: Small Business Owner Managing Supply Interruption

- Situation: A boutique owner needs 15,000 INR to secure a limited material shipment before client billing clears.

- Mistake: Using a high-interest personal cash advance app without calculating the impact on their profit margins.

- Better Action: Using a dedicated merchant cash credit line linked directly to their business point-of-sale platform.

- Learning: Match your borrowing tool to your specific cash flow model to protect your business profits.

Example 3: Freelancer Covering Utility Delays

- Situation: A graphic designer faces a 6,000 INR energy bill while waiting for a client invoice to settle.

- Mistake: Ignoring the bill entirely, which leads to service disconnection and a steep reconnection penalty.

- Better Action: Using a regulated “Buy Now, Pay Later” line to pay the bill, then clearing the balance as soon as the client pays.

- Learning: Short-term credit is highly effective for timing mismatches, provided the repayment source is locked in.

Example 4: New Investor Dealing with Misaligned Liquidity

- Situation: An investor needs 5,000 INR for an urgent medical cost and considers selling long-term stock investments during a market drop.

- Mistake: Cashing out their investments early, locking in a permanent financial loss.

- Better Action: Taking a short-term micro-loan, keeping their investments intact, and paying off the loan with their next salary.

- Learning: A small loan can protect your long-term investments from being disrupted by temporary cash needs.

Example 5: Student Managing Mandatory Exam Registration

- Situation: A working student needs 3,500 INR for an exam fee that must be paid before their monthly stipend arrives.

- Mistake: Turning to unverified online lenders that charge high daily compounding fees.

- Better Action: Utilizing an official student credit line backed by their university or a major public bank.

- Learning: Always check for specialized, community-focused credit options before looking at commercial lending apps.

Two Useful Tables for Better Understanding

Table 1: Structural Comparison of Short-Term Borrowing Options

| Borrowing Method | Typical Approval Speed | Relative Cost Structure | Primary Risk Factor | Optimal Use Case |

| Bank Overdraft Line | Instant (If pre-approved) | Low to Medium (Annualized Interest) | Variable Interest Rates | Account balance mismatches for salaried workers. |

| Regulated Fintech App | 10 to 60 Minutes | Medium to High (Processing Fees) | High Late-Payment Penalties | Urgent medical or logistical emergencies. |

| Employer Salary Advance | 2 to 5 Business Days | Very Low (Often Interest-Free) | Internal Workplace Processes | Planned expenses late in the monthly cycle. |

| Peer-to-Peer Network | 24 to 48 Hours | Medium (Platform Fees) | Variable Investor Approval | General liquidity shortfalls with stable histories. |

Table 2: The Cost Impact of Late Repayments

| Phase of Repayment Timeline | Added Fee Type | Credit Bureau Impact | Operational Result |

| On-Time Settlement | No Extra Charges | Score increases over time. | Account closes cleanly with a positive credit note. |

| 1 to 3 Days Overdue | Minor Grace Fees | Negligible initial risk. | Automated notifications and payment reminders start. |

| 4 to 30 Days Overdue | Flat Late Penalties + Compound Interest | Score decreases immediately. | Digital access is frozen; collections communications begin. |

| Beyond 31 Days Overdue | Heavy Default Penalties | Severe long-term damage. | Debt is routed to official recovery specialists. |

Tools, Methods, and Frameworks Readers Can Use

The 24-Hour Cooling-Off Rule

When you feel the urge to borrow money for a non-medical expense, force yourself to wait 24 hours. This break separates urgent emotional wants from true, immediate needs, helping you avoid impulsive, high-cost debt.

Digital EMI and APR Calculators

Before accepting a loan, plug the figures into an independent Annual Percentage Rate (APR) tool. Enter the exact cash amount that will land in your bank account against the total amount you are required to pay back. This calculation reveals the true cost of the loan, stripping away any confusing marketing language.

Debt-to-Income Framework

Keep your total monthly debt payments (including any small cash loans) under 30% of your take-home income.

$$\text{Debt-to-Income Ratio} = \left( \frac{\text{Total Monthly Debt Payments}}{\text{Net Monthly Take-Home Pay}} \right) \times 100$$

If your calculation crosses this 30% threshold, stop borrowing immediately. This is a clear sign that you need to adjust your core budget rather than taking on more short-term credit.

Expert Tips to Make Better Decisions

- Prioritize Regulated Institutions: Only borrow from platforms explicitly tied to verified banks or licensed financial entities.

- Confirm the Final Disbursal Amount: Always verify the exact amount of cash that will drop into your account after all upfront fees are deducted.

- Keep an Independent Record: Store your own copies of your loan closure certificates and transaction receipts; do not rely solely on a lending app’s dashboard.

- Build a Dedicated Emergency Buffer: Work toward saving a small cash cushion—even a modest fund can help you avoid the need for micro-loans in the future.

- Review App Permissions Manually: Go into your phone’s settings and turn off unnecessary permissions (like contacts and photos) for financial apps.

- Align Your Due Date with Your Payday: Schedule your loan payments for 2 to 3 days after your regular expected salary date to account for any payroll delays.

- Opt for Fixed Reducing Rates: Avoid flat-rate loans where interest is calculated on the original principal even as you pay it down.

- Never Use Micro-Credit for Leisure: Keep your borrowing strictly limited to non-negotiable emergencies.

- Check Your Credit Report Regularly: Use official, free credit portals to review your file quarterly and ensure closed loans are marked correctly.

- Avoid Auto-Renewal Features: Do not opt into programs that automatically roll your debt over into a new loan cycle once the term ends.

Case Studies: How Better Understanding Changes Decisions

Case Study 1: The Impact of Rushed Digital Borrowing

- Profile: A customer support executive earning 25,000 INR monthly.

- Situation: Faced a sudden 5,000 INR phone repair cost.

- Wrong Approach: Downloaded an unverified loan app that promised instant cash, skipping the terms. They were hit with a hidden 20% weekly compound fee and aggressive collection calls.

- Better Approach: They should have checked their primary bank account for a pre-approved micro-overdraft or requested a short-term advance from their employer.

- Result: By choosing the rushed app, they ended up paying back over 12,000 INR. A regulated alternative would have cost less than 300 INR in total interest.

- Key Takeaway: Speed should never take priority over checking a lender’s regulatory safety and fee structure.

Case Study 2: Managing Business Inventory Shortfalls Safely

- Profile: A home bakery owner managing a spike in holiday orders.

- Situation: Needed 12,000 INR to purchase bulk ingredients before customer payments cleared.

- Wrong Approach: Taking out a high-interest personal consumer loan meant for retail shopping.

- Better Approach: Using a formal, short-term micro-business credit line with terms structured around commercial invoice timelines.

- Result: The business line allowed them to clear the debt cleanly within 30 days using their holiday sales revenue, protecting their profit margins.

- Key Takeaway: Match the type of loan to your specific cash flow model to keep your borrowing safe and predictable.

Case Study 3: The Benefits of an Emergency Cash Cushion

- Profile: A freelance software developer with fluctuating monthly income.

- Situation: Faced a 7,000 INR medical expense during a month when client payments were delayed.

- Wrong Approach: Taking out multiple overlapping micro-loans from different mobile apps to bridge the gap.

- Better Approach: Using a small, dedicated emergency cash buffer built during high-income months, avoiding new debt entirely.

- Result: By relying on their own savings buffer, they navigated the dry spell smoothly without impacting their credit score or paying interest.

- Key Takeaway: Building a personal cash reserve is the ultimate defense against the costs and risks of short-term borrowing.

Risk Awareness: What Readers Must Check First

┌───────────────────────────┐

│ Assess Borrowing Risks │

└─────────────┬─────────────┘

│

┌──────────────────────────┼──────────────────────────┐

▼ ▼ ▼

┌─────────────────┐ ┌─────────────────┐ ┌─────────────────┐

│ Credit Risk │ │ Regulatory Risk │ │ Data Privacy │

│ Missed payments │ │ Unlicensed apps │ │ Aggressive apps │

│ damage score │ │ inflate costs │ │ compromise data │

└─────────────────┘ └─────────────────┘ └─────────────────┘

- Credit Profile Impact: Every single late payment on a micro-loan is reported to credit bureaus. This can lower your credit score and make it much harder to qualify for major loans, like a home or car loan, in the future.

- Regulatory Compliance Risks: Unlicensed lending apps often operate outside consumer protection laws. They can arbitrarily inflate interest rates, add unexpected fees, and use aggressive collections tactics.

- Data Privacy Exposures: Some digital lending platforms use invasive terms to scrape your smartphone data. This can expose your private information, contact lists, and location history to external networks.

Checklist Before Taking Action

- I have verified that the lender is fully registered and regulated by national financial authorities.

- I have calculated the true cost of the loan using the complete Annual Percentage Rate (APR), including all processing fees.

- I have reviewed my upcoming monthly budget to ensure I have enough free cash flow to clear the balance on time.

- I have confirmed the exact amount of cash that will be deposited into my account after all upfront fees are deducted.

- I have carefully read the rules and penalties regarding late payments and default charges.

- I have turned off unnecessary smartphone permissions (like access to contacts and photos) in my device settings.

- I have set up an automated payment instruction or auto-debit tied directly to my payday to avoid missing the deadline.

Using a structured checklist before you sign a loan agreement removes emotion from the process, ensuring you use short-term credit as a safe, calculated financial utility.

Strategic Insights for Better Decision-Making

Analyzing the Total Cost Profile

When looking at small cash loans, do not judge the cost based on the initial dollar or rupee amount. A 400 INR processing fee on a small 4,000 INR loan means you are paying a 10% premium upfront before any interest is even applied. Always calculate your borrowing costs using percentages relative to the total loan size to understand the real financial impact.

Avoiding the Debt Rollover Trap

Some lenders offer an option to “extend” or “roll over” your loan for a small fee if you cannot pay on time. While this delays the due date, it adds a new layer of processing fees and compound interest to your original balance. This process can quickly snowball a minor loan into an unmanageable financial burden. Treat your initial repayment deadline as absolute and non-negotiable.

Key Terms Explained for Beginners

- Annual Percentage Rate (APR): The total cost of borrowing money expressed as a yearly percentage. It combines the base interest rate with all upfront processing fees and administrative charges.

- Reducing Interest Rate: An interest calculation method where charges apply only to the remaining unpaid loan balance, rather than the initial amount borrowed. This approach costs less over time than flat-rate calculations.

- Processing Fee: A one-time administrative charge deducted by the lender upfront to cover the costs of reviewing and setting up your loan.

- Default Status: The official financial classification triggered when a borrower fails to make payments according to the agreed-upon schedule for an extended period.

- Debt-to-Income Ratio: A personal finance metric calculated by dividing your total monthly debt payments by your net monthly take-home pay, expressed as a percentage.

- Credit Bureau: A certified national institution that tracks, aggregates, and reports consumer credit histories and payment behaviors to lenders.

- NBFC (Non-Banking Financial Company): A financial institution that offers loan products and credit facilities but does not hold a full banking license and is regulated by national authorities.

- Principal Amount: The core sum of money originally borrowed from the lender, before any interest charges or late fees are added.

- Prepayment Penalty: An extra fee charged by some lenders if a borrower pays off their outstanding loan balance ahead of the official scheduled deadline.

- Grace Period: A short, specified window of time after the official due date during which a payment can be made without triggering late penalties or credit score damage.

Who Should Read This Blog

- Salaried Employees: Individuals looking to manage unexpected, mid-month expenses safely without disrupting their core savings or monthly budgets.

- Small Business Owners: Managers and entrepreneurs who need short-term cash to handle temporary supply chain or inventory costs without hurting their profit margins.

- Freelancers and Gig Workers: Independent professionals with variable monthly income who need safe ways to balance their cash flow between client payments.

- Financial Beginners: Anyone looking to build a strong credit history while learning how to evaluate loan terms and avoid common debt traps.

Frequently Asked Questions

What does it mean to borrow small cash responsibly?

It means taking out short-term micro-loans only for genuine financial emergencies, verifying that your lender is fully regulated, understanding the total cost (including all fees), and having a clear plan to pay the balance back on time.

How do I check if a small cash loan app is safe?

Review the app’s official documentation to identify its licensed partner bank or Non-Banking Financial Company (NBFC). Cross-check these names against the official registries provided by your national financial regulator.

Will borrowing a small amount affect my credit score?

Yes. Every micro-loan is reported to credit bureaus. Paying the loan back on time helps build a positive credit history, while missing deadlines will immediately damage your credit score.

What is a normal interest rate for a small cash loan?

Because micro-loans are processed quickly without requiring collateral, their interest rates are higher than long-term loans. Regulated apps typically charge annualized rates ranging from 18% to 36%, often accompanied by upfront processing fees.

What should I do if I cannot pay my loan on time?

Contact your lender immediately before you miss the deadline. Many regulated institutions can offer a structured repayment plan or an official extension, which is far better than skipping the payment and facing steep penalties.

Are “zero-interest” small loans actually free?

Usually, no. While the promotional interest rate might be zero, these loans often include high, non-refundable upfront processing fees or account setup costs that make up for the interest.

Can a lender access my phone contacts?

Regulated lending apps must follow strict consumer privacy laws and typically do not require access to your personal contacts or photos. Avoid any platform that demands broad access to your personal data as a condition for approval.

What is the difference between a flat interest rate and a reducing interest rate?

A flat rate calculates interest based on the entire original loan amount for the whole term. A reducing rate calculates interest only on the remaining unpaid balance, making it a much cheaper option as you pay down the debt.

How can I avoid borrowing small cash in the future?

Set up a small, dedicated emergency fund by automatically saving a small portion of your income each month. Even a modest cash cushion can help you cover unexpected costs without needing to borrow.

Is it a good idea to use one loan app to pay off another?

No. Using new debt to pay off old loans creates a dangerous, compounding cycle of debt that increases your overall costs and can quickly overwhelm your personal budget.

What are the most common hidden fees in micro-loans?

Pay close attention to upfront documentation fees, account maintenance charges, prepayment penalties, and high flat rates for late payments.

What should I do immediately after paying off a small loan?

Check your account to confirm the balance is zero, download your official loan closure certificate from the lender, and review your credit report a few weeks later to ensure the account is marked as settled.

Conclusion and Next Steps

Borrowing small cash responsibly is a valuable skill that requires careful planning, a clear understanding of loan terms, and structural discipline. Micro-loans can be highly effective tools for managing unexpected financial emergencies, but they should never be treated as an extension of your regular spending money or used to cover everyday budget deficits. Rushing into a loan without checking the details can quickly turn a temporary cash crunch into a long-term debt problem.

Your immediate next step is to evaluate your current financial situation. Take a close look at your monthly income, map out your mandatory living expenses, and look for small areas where you can start building a modest emergency savings buffer. If you do find yourself needing to borrow short-term cash, use the step-by-step frameworks and checklists in this guide to protect your data, minimize your costs, and keep your credit score healthy.