Introduction

Month-end money pressure becomes stressful when urgent expenses arrive before salary. Imagine a typical Tuesday afternoon when a sudden medical emergency, an unheralded home repair, or an immediate family obligation demands a significant cash outlay. For many salaried professionals, your monthly paycheck is carefully allocated toward rent, groceries, utility bills, and existing investment plans. There is rarely a massive cushion of idle cash sitting in a checking account. When a financial shock hits, turning to external funding becomes a practical necessity.

However, many beginners enter the borrowing market with high anxiety and limited preparation. They often feel confused when different lenders display vastly different interest rates, processing terms, and documentation demands. This panic often leads to a frantic, unorganized application process. Desperate times cause individuals to apply to multiple banks and digital lending apps simultaneously, hoping that someone will say yes.

This approach can cause significant financial damage. Every formal loan application triggers a “hard inquiry” on your credit file, which can rapidly lower your credit score and flag you as a high-risk, desperate borrower. Furthermore, a lack of clarity regarding eligibility criteria can lead to immediate loan rejections. These rejections cost valuable hours during a crisis when time is the most critical resource.

This comprehensive guide is designed to clarify the process by providing an emergency loan eligibility checklist for salaried employees. We will explain what lenders look for, why certain financial metrics matter, and how you can position your profile to secure rapid, low-cost approvals. Whether you work for a major corporation, a small boutique agency, or a public sector institution, this blog will provide you with practical financial knowledge.

Moving forward with a logical, systematic plan is far better than making impulsive, fear-based financial moves. By understanding your eligibility before talking to a lender, you can take control of the conversation, minimize borrowing costs, and protect your financial health.

Understanding Emergency Loans in Simple Words

An emergency loan is a short-term personal loan designed to provide rapid access to capital during unexpected situations. Unlike structured financing like home or auto loans, these funds are unsecured, meaning you do not need to pledge assets like property, gold, or stocks as collateral. Lenders evaluate your ability to repay the debt based on your regular monthly salary, your credit history, and your employment stability.

In real life, people search for these loans because speed is a top priority. Traditional bank loans can take weeks to process due to manual underwriting and asset verification. In contrast, digital emergency loans focus on automated verification systems to approve and disburse funds within a few hours, or even minutes.

How It Works in Practice

Think of an emergency loan as a financial bridge. Suppose your car’s transmission breaks down completely, resulting in an unexpected repair bill. Your next salary payment is two weeks away, and your savings cannot cover the full amount.

You apply for a short-term personal loan, the lender reviews your income and credit profile digitally, approves the funds, and deposits the capital into your account. Once your regular monthly salary arrives, you begin paying back the borrowed amount through monthly Fixed Installments (EMIs) over an agreed timeline.

Common Misunderstanding

The Myth: Many beginners believe that having a high salary guarantees instant loan approval, regardless of their past financial habits.

The Reality: A high income is only one piece of the puzzle. If a professional earns a substantial salary but spends nearly all of it on expensive lifestyle choices or carries heavy credit card balances, a lender may still reject the application due to poor repayment habits or an excessive debt load.

Practical Takeaway

An emergency loan should be treated as a targeted financial tool for unpredictable crises, not an extension of your regular monthly income for casual spending.

Why Knowing Your Loan Eligibility Is Crucially Important

Understanding your eligibility beforehand has a direct impact on your real-life financial choices and long-term stability. When a financial crisis hits, emotional decision-making often overrides logical analysis. If you know exactly where you stand in the eyes of a lender, you can avoid common pitfalls that damage your personal finances.

+-------------------------------------------------------------+

| BENEFITS OF PRE-AUDITING ELIGIBILITY |

+-------------------------------------------------------------+

| 1. Protects Credit Score (Avoids multiple hard inquiries) |

| 2. Saves Critical Time (Saves hours during a real crisis) |

| 3. Boosts Bargaining Power (Helps negotiate lower rates) |

| 4. Prevents Over-Borrowing (Keeps EMIs within actual budget)|

+-------------------------------------------------------------+

The Impact Across Financial Pillars

- Savings and Emergency Funds: Knowing your loan eligibility prevents you from making the mistake of entirely emptying your long-term retirement savings or liquidating long-term investments during a short-term cash crunch.

- Borrowing Costs: Clear eligibility allows you to look past high-cost, predatory lenders and qualify for institutional personal loans with competitive interest rates.

- Risk Awareness & Discipline: It forces you to look closely at your fixed monthly commitments, preventing you from taking on a heavy debt burden that could ruin your future monthly budgets.

A Practical Scenario

Consider two colleagues, Rohan and Vikram, who both face a sudden medical billing gap. Rohan does not check his eligibility and applies to four different mobile apps within an hour. His credit profile receives four hard hits, his score drops by 35 points, and three apps reject him due to his brief tenure at his current job. The fourth app approves him at an expensive 28% annual interest rate.

Vikram takes ten minutes to review his basic eligibility criteria. He notes his steady two-year employment history and solid credit score, chooses a single reputable lender that fits his profile, and receives approval at a manageable 13% interest rate. This demonstrates how a clear understanding of eligibility leads to better, more deliberate choices.

The Real Problem Salaried Borrowers Face in a Financial Crisis

The true challenge for salaried employees during an emergency is not a lack of available lenders. The actual issue is navigating a high-volume, confusing digital lending market while under intense psychological stress.

Core Challenges Faced by Borrowers

- Confusing Online Advice: Searching for urgent financing online yields millions of results filled with aggressive marketing terminology. Borrowers are hit with terms like “instant approval,” “zero documentation,” and “no credit check loans.” This leaves beginners struggling to separate legitimate, safe financial institutions from predatory lending platforms.

- The “Zero-Research” Trap: Because money is needed immediately, borrowers rarely take the time to compare lenders or read the underlying terms and conditions. They often accept the very first loan offer presented to them, ignoring excessive processing fees, prepayment penalties, and high default interest rates.

- Ignoring the Debt-to-Income Ratio: Borrowers frequently look only at the total loan amount offered, rather than evaluating whether their monthly salary can handle the resulting EMI. This lack of planning leads to a cycle of structural debt, where individuals must take out new loans just to pay off old ones.

- Over-reliance on Unverified Advice: Many young professionals depend entirely on casual social media content or unverified peer advice for financial steps, completely missing the structured rules of institutional credit evaluation.

This breakdown highlights that lenders are looking for specific, objective data indicators before they deploy capital. Showing that you understand this reality is the first step toward securing a safe, affordable loan.

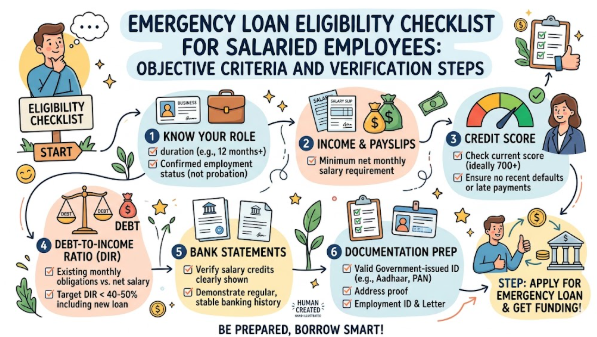

How to Verify and Improve Your Emergency Loan Eligibility Step by Step

Step 1: Conduct a Credit Score Self-Audit

- What it means: Checking your current credit score through an official credit bureau platform.

- Why it matters: Lenders check this number first to judge your past repayment discipline. A score above 750 opens access to lower interest rates.

- How to apply it: Use an authorized digital portal to pull your credit report. Check for any reporting errors, such as loans you have already closed that are still marked as active.

- Practical example: An employee pulls her report and finds a small, forgotten credit card balance of $15 that is marked as overdue, causing her score to sit at 680.

- Common mistake: Applying for an urgent loan without checking your score, assuming it must be fine because your salary is high.

- Better approach: Check your credit report every quarter to catch and fix reporting errors before an actual emergency happens.

Step 2: Calculate Your Debt-to-Income Ratio

- What it means: Finding the percentage of your monthly net income that currently goes toward paying off existing debts.

- Why it matters: Lenders rarely allow your total monthly debt payments (including the new loan) to exceed 45% to 50% of your take-home pay.

- How to apply it: Add up all your active monthly credit card payments and EMIs, then divide that total by your net monthly take-home salary.

- Practical example: An employee earns $4,000 a month after taxes. His current car loan and credit card bills equal $1,200. His current ratio is 30%, leaving room for an emergency loan payment.

- Common mistake: Requesting a high loan amount that pushes your total monthly debt payments above 60% of your income, which triggers an automatic system rejection.

- Better approach: Keep your baseline debt payments below 30% of your income during normal times so you have borrowing room for emergencies.

Step 3: Verify Length of Employment and Employer Category

- What it means: Confirming that you meet the minimum time-on-the-job requirements set by major lenders.

- Why it matters: Lenders view individuals working at established corporate firms or government bodies as lower risk. They typically require at least 6 months with your current employer and 12 months of total working history.

- How to apply it: Gather your official employment contract, your confirmation letter, and your official corporate email credentials to streamline verification.

- Practical example: A worker who changed jobs just two weeks ago may face rejections from standard banks, requiring him to seek out specialized lenders that look at overall industry experience rather than time at your current company.

- Common mistake: Assuming that a high-paying job at a brand-new, unlisted startup carries the same compliance weight as a mid-level job at an enterprise firm.

- Better approach: If you recently changed jobs, be ready to provide your formal relieving letter and employment records from your previous firm to prove continuous income.

Step 4: Organize Your KYC and Income Documentation

- What it means: Getting your Know Your Customer (identity and address proof) documents and income proofs ready before starting an application.

- Why it matters: Missing or mismatched documents slow down the underwriting process, turning a 2-hour approval into a multi-day delay.

- How to apply it: Create a secure digital folder containing your government ID, tax filing records, your company ID card, and your official salary account statements for the last six months.

- Practical example: A borrower stores clear, digital PDF copies of his bank statements on his phone, allowing him to upload them immediately when requested by a digital lender.

- Common mistake: Uploading blurry smartphone photos of documents or truncated online banking screenshots that lack the bank’s official logo and account details.

- Better approach: Download clean, original digital PDF statements directly from your bank’s portal to ensure smooth processing by automated verification systems.

Step 5: Match Your Financial Profile to the Right Lender

- What it means: Researching which banks, financial institutions, or digital apps specialize in your specific credit profile.

- Why it matters: Premium banks focus on prime borrowers (those with excellent credit and high corporate tiers), while alternative digital lenders assist individuals with average credit scores.

- How to apply it: Check the transparent eligibility guidelines listed on various lender websites before hitting the submit button.

- Practical example: A borrower with a 670 credit score avoids premium international banks and instead applies to an established domestic financial institution that serves near-prime borrowers.

- Common mistake: Applying to premium institutions with an average credit profile, resulting in a rejection that further lowers your credit score.

- Better approach: Use neutral financial comparison platforms to identify the specific lenders that actively accept applicants matching your income level and credit range.

Key Factors That Influence Urgent Loan Approvals

When an evaluation system reviews an emergency loan application from a salaried professional, it looks closely at several core factors. Understanding these elements helps you see your application from the lender’s perspective.

1. Interest Rate Framework

The interest rate determines the overall cost of your borrowed money. For unsecured emergency capital, rates can vary from 11% to over 35% annually. Lenders calculate this rate using risk-based pricing: the higher your credit score and job stability, the lower the interest rate you will receive.

2. Equated Monthly Installment (EMI) Structure

Your EMI is the fixed amount of money you must pay back each month. It includes a portion of the original loan balance plus interest. It is vital to check that this monthly obligation fits into your current budget without forcing you to cut back on core necessities like rent, food, or healthcare.

3. Credit Score Thresholds

Your credit score is a three-digit summary of your past borrowing behavior.

- 750 or higher: Excellent profile. Qualifies for fast approvals and the lowest interest rates.

- 650 to 740: Moderate profile. Qualifies with standard lenders, though rates may be slightly higher.

- Below 650: High-risk profile. May face rejections at major institutions, requiring specialized alternative financing.

4. Processing Fees and Onboarding Costs

Lenders charge a processing fee to set up your loan account, usually ranging from 1% to 5% of the total loan amount.

Important Note: This fee is typically deducted directly from the money sent to your account. For example, if you are approved for a $5,000 loan with a 3% processing fee, you will receive $4,850 in your bank account, but you are still responsible for paying back the full $5,000 plus interest.

5. Hidden Administrative Charges

Always check the fine print for extra costs like document verification fees, loan management charges, and digital platform fees. Reputable lenders maintain full transparency, whereas predatory platforms often hide these operational charges within complex terms and conditions.

6. Loan Tenure Options

Tenure refers to the total amount of time you have to repay the loan, typically ranging from 3 to 36 months for emergency personal loans. A longer tenure reduces your individual monthly EMI payment, but it increases the total interest you pay over the life of the loan.

7. Prepayment and Early Closure Rules

If you receive a bonus or extra cash, you may want to pay off your loan early. Many lenders charge a prepayment penalty (often 2% to 5% of the remaining balance) to recover the interest income they lose when you pay early. Always check for lenders that offer zero foreclosure charges after a set number of initial monthly payments.

Detailed Breakdown of Emergency Borrowing for Salaried Professionals

Borrowing funds during a crisis requires a careful balance between immediate financial relief and long-term financial safety. Unsecured personal loans are effective tools when used properly, but they can become a serious financial burden if mismanaged.

When Emergency Borrowing Makes Sense

An emergency loan is appropriate when facing time-sensitive, non-discretionary expenses that impact your health, safety, or employment. Examples include covering sudden medical bills not fully met by insurance, paying for urgent home repairs like a leaking roof, or fixing a vehicle needed for your daily commute. In these situations, the cost of borrowing is justified by resolving a critical problem immediately.

When Emergency Borrowing Should Be Avoided

Do not use emergency loans for non-essential purchases or discretionary lifestyle choices. Taking out a high-interest personal loan to pay for an expensive vacation, upgrade consumer electronics, cover holiday shopping, or fund speculative investments like day trading is highly risky. Using short-term debt for non-essential items creates long-term financial pressure on your monthly salary.

The Long-Term Impact of Late Payments

Missing an EMI payment has serious, cascading financial consequences:

[Missed EMI Payment]

│

▼

[Late Fees & Penalties Applied]

│

▼

[Negative Report Sent to Credit Bureaus]

│

▼

[Credit Score Drops Significantly]

│

▼

[Future Loans Denied or Offered at Extreme Rates]

To protect your financial health, always check the exact terms and conditions before signing a loan agreement. Genuine emergency borrowing requires clear comparison shopping, transparent pricing, and a realistic plan to pay back the debt using your future salaries.

Common Mistakes Beginners Make When Applying for Emergency Capital

When navigating an unexpected cash shortage, avoiding errors is just as important as meeting eligibility criteria. Here are the most common mistakes beginners make, along with better approaches to keep your finances secure.

1. Applying to Multiple Lenders Simultaneously

- Why it happens: Out of panic, borrowers submit forms to five or six different banks at the same time, hoping for a fast approval.

- Why it is risky: Every submission triggers an independent hard inquiry on your credit report. This sudden spike in credit checks signals financial distress to underwriting systems, lowering your score and increasing your chances of rejection.

- Better approach: Use online comparison tools to find the single lender that best matches your credit profile, then apply to that specific institution first.

2. Ignoring the Fine Print and Hidden Charges

- Why it happens: The borrower is in a rush to receive the funds and quickly clicks through digital terms and conditions pages without reading them.

- Why it is risky: You may overlook high bounce fees, steep late payment penalties, or hidden monthly service charges that significantly increase the actual cost of your loan.

- Better approach: Take five minutes to read the formal loan summary document, focusing closely on the annual percentage rate (APR), processing fees, and foreclosure terms.

3. Borrowing Far More Than Necessary

- Why it happens: A lender offers an eligible professional a maximum loan amount of $10,000, even though the actual emergency bill is only $3,000. The borrower accepts the full amount to buy non-essential items.

- Why it is risky: Borrowing unnecessary funds increases your monthly EMI obligations and wastes money on interest fees for capital you did not actually need.

- Better approach: Borrow only the exact amount required to handle the immediate crisis, leaving the rest of your borrowing capacity clear.

4. Sharing Sensitive Personal and Financial Information on Unverified Sites

- Why it happens: Desperate for capital, borrowers enter their personal details, bank login info, or identity numbers into unverified online portals or unlisted mobile applications.

- Why it is risky: This exposes you to identity theft, phishing scams, and predatory networks that use your information for financial fraud.

- Better approach: Only enter your sensitive data directly on official, encrypted corporate websites or verified mobile applications from recognized financial institutions.

“Don’t Do This” Safety Checklist

- Do not accept loan offers from lenders that refuse to provide a formal, written loan agreement.

- Do not provide upfront cash payments to brokers or agents who promise “guaranteed loan approval.”

- Do not link your primary salary account to automated repayment systems without verifying the exact monthly deduction dates.

- Do not use high-interest emergency capital to pay off regular monthly lifestyle bills or credit card debt.

- Do not hide existing debts or alternate sources of income when filling out your formal loan application.

Practical Real-Life Examples of Urgent Borrowing Situations

Example 1: Salaried Employee Managing Sudden Medical Bills

- Situation: Rajesh faces an unexpected medical procedure costing $2,500 that is not covered by his basic employer health insurance plan.

- The Mistake: He applies for three separate credit cards online within an afternoon, hoping to split the bill, which causes his credit score to drop.

- Better Action: He gathers his last three salary slips, applies to a single reputable personal loan lender offering a specialized medical financing plan, and secures the money within 24 hours.

- Learning: Always look for focused financial options and keep your application process clean to protect your credit history.

Example 2: Navigating Urgent Car Repairs for Daily Commuting

- Situation: Priya’s car engine breaks down, resulting in an unexpected $1,200 repair cost necessary for her to get to work each day.

- The Mistake: She borrows money from an unverified, high-interest mobile lending app without reviewing their steep processing fees.

- Better Action: She uses her bank’s pre-approved digital personal loan portal to get a transparent, short-term loan at an established interest rate.

- Learning: Check with your primary banking partner first for pre-approved credit options before looking at external lending platforms.

Example 3: Fixing Major Home Damage During the Rainy Season

- Situation: Intense storms cause a major water pipe break in Amit’s home, requiring an immediate $3,000 repair to prevent structural damage.

- The Mistake: He decides to delay the repair while trying to save cash from his next few paychecks, which allows the water damage to worsen.

- Better Action: He reviews his eligibility checklist, confirms his debt ratio is low, and secures a 12-month personal loan to fix the issue right away.

- Learning: Addressing a physical emergency early using affordable credit prevents a small issue from turning into a massive expense later.

Example 4: Managing Mid-Month Family Cash Emergencies

- Situation: A family emergency requires Sunita to send $1,500 to her parents living in another town mid-month.

- The Mistake: She withdraws the cash by taking a cash advance from her credit card, ignoring the steep daily interest charges and cash advance fees.

- Better Action: She takes out a short-term emergency personal loan with an flexible 6-month repayment schedule, avoiding high credit card fees.

- Learning: Avoid credit card cash advances for large amounts; short-term personal loans offer much lower overall borrowing costs.

Example 5: Handling Job Transition Gaps and Overdue Bills

- Situation: Vikram transitions between corporate jobs and faces a 15-day delay in receiving his first monthly paycheck, putting his rent payment at risk.

- The Mistake: He skips his rent payment entirely without talking to his landlord, while also defaulting on his ongoing car loan EMI.

- Better Action: He uses an alternative short-term financing option to cover his core bills on time, then pays off the full balance as soon as his new salary arrives.

- Learning: Maintaining a clean credit record during job transitions requires proactive planning and open communication with your creditors.

Comparative Data Tables for Informed Financial Decision-Making

Table 1: How Credit Scores Impact Emergency Loan Eligibility and Terms

| Credit Score Range | Eligibility Level | Average Interest Rate Range | Processing Speed | Typical Documentation Needs |

| 750 and Above | Excellent / High Approval | 11.0% – 14.5% Annual | Instant (Automated) | Basic ID + Last 3 Months Bank Statements |

| 680 to 749 | Moderate / Standard Approval | 15.0% – 22.0% Annual | Same Day Review | Standard Income Verification + Company Details |

| 600 to 679 | Conditional / Review Required | 23.0% – 32.0% Annual | 1 to 2 Business Days | Detailed Salary History + Tax Returns + Guarantor |

| Below 600 | High Risk / Frequent Rejections | Above 33% (Alternative Only) | Multi-Day Manual Audit | Full Financial Review / Collateral required by most |

Table 2: Comparing Emergency Capital Sources for Salaried Professionals

| Funding Source Type | Average Approval Speed | Interest Cost Profile | Impact on Credit Score | Primary Structural Risk |

| Bank Emergency Loan | 4 to 24 Hours | Low to Moderate (11%-18%) | Positive if paid on time | Strict employment and minimum income limits |

| Digital Lending App | 10 Minutes to 2 Hours | High (18%-36%) | High impact on hard checks | Hidden operational fees and automatic penalties |

| Credit Card Cash Advance | Instant at ATM | Extreme (36%-48% + Fees) | Increases credit utilization | High compound interest charges starting day one |

| Peer-to-Peer Platform | 1 to 3 Business Days | Variable based on platform | Reported to major bureaus | Platform processing and onboarding delays |

Tools, Methods, and Frameworks for Pre-Loan Assessment

Before filling out an online application, using specific financial tools and methods can help you verify your eligibility and avoid costly mistakes.

1. Digital EMI Calculator

An online EMI calculator allows you to enter a loan amount, interest rate, and tenure to see your exact monthly payment. Using this tool before applying helps you experiment with different repayment timelines. This ensures your monthly payment fits into your budget before you sign any agreements.

2. Net Disposable Income Tracking Sheet

This approach involves listing your total net monthly salary and subtracting all fixed expenses like rent, utilities, insurance, food, and existing loan payments. The money left over is your net disposable income.

Crucial Rule: Your new emergency loan EMI should never consume more than 50% of this remaining disposable income. Following this rule protects you from running out of cash for daily expenses mid-month.

3. Credit Bureau Dispute Portal

This is a formal online method provided by recognized credit tracking bureaus to help consumers correct mistakes on their credit history. If you find errors on your report during your self-audit, using these portals to update your data can improve your credit score before you apply for a loan.

Expert Tips to Make Better Urgent Borrowing Decisions

- Verify the Lender’s License: Always check that the platform you choose is a licensed financial institution or an authorized digital partner of a regulated bank.

- Match the Loan Timeline to Your Capital: Choose a repayment tenure that keeps your monthly payments manageable without extending your debt longer than necessary.

- Keep an Eye on the Total Cost (APR): Do not just focus on the headline interest rate. Look at the Annual Percentage Rate (APR), which includes both interest and processing fees to show the true cost of the loan.

- Communicate Early with Existing Creditors: If an unexpected crisis leaves you short on cash, talk to your current lenders. They may offer a temporary payment pause, which is much better than missing an EMI.

- Avoid Loans for Speculative Investments: Never take out an emergency loan to buy volatile assets like cryptocurrencies or individual stocks, as losing that money leaves you with a heavy debt and no way to pay it back.

- Protect Your Salary Account: Make sure you keep enough money in your main account on your monthly deduction date to avoid expensive auto-debit bounce fees.

- Ask for a Full Breakdown of Fees: Request a clear, written list of all fees from your loan officer before final approval to ensure there are no hidden surprises.

- Check the Prepayment Rules: Choose a loan that allows you to make extra payments or pay off the balance early without heavy penalties.

- Keep Personal Copies of Loan Documents: Save digital copies of your approved loan agreement, repayment schedule, and final closure letters in a secure folder for your own records.

- Build a Dedicated Emergency Fund: Once your immediate financial crisis is resolved, start saving a small portion of your monthly income into a dedicated emergency fund to reduce your reliance on debt in the future.

Case Studies: How Pre-Application Audits Change Financial Outcomes

Case Study 1: The Impact of Multiple Blind Applications

- Profile: Marketing Coordinator at an e-commerce firm.

- Situation & Problem: Needed $2,000 for an urgent dental procedure mid-month with no personal savings available.

- The Wrong Approach: Out of panic, he applied to five different digital loan apps within two hours without checking his credit history or reviewing eligibility terms.

- The Result: His credit report received five hard inquiries in one day, causing his score to drop from 710 to 665. Three apps rejected him instantly due to the sudden spike in inquiries, and the remaining apps offered him high interest rates near 30%.

- Key Takeaway: Blindly submitting multiple applications damages your credit profile and drives up the cost of borrowing during a crisis.

Case Study 2: Using a Pre-Application Eligibility Checklist Successfully

- Profile: Software Quality Analyst at a mid-tier IT company.

- Situation & Problem: Faced a sudden $3,500 home repair bill due to an unexpected water line break.

- The Better Approach: She paused, checked her credit score (765), gathered her last six months of original bank PDFs, and calculated her debt-to-income ratio (currently 15%). She identified a single bank that specialized in her employment tier and submitted a single targeted application.

- The Result: The system approved her application automatically within three hours, granting her a competitive 11.5% interest rate with a transparent 1.5% processing fee.

- Key Takeaway: Taking time to review your eligibility allows you to secure low-cost institutional funding quickly and safely.

Case Study 3: Overcoming an Average Credit History Safely

- Profile: Operations Supervisor at a regional logistics company.

- Situation & Problem: Needed $1,500 for family emergency travel expenses. His credit score sat at 640 due to past credit card payment delays.

- The Better Approach: He avoided premium banks where his application faced automatic rejection. Instead, he searched for regulated alternative finance platforms that serve near-prime borrowers, presenting clear evidence of his steady three-year job history.

- The Result: The lender approved a 12-month loan at a 22% interest rate. He accepted the higher cost, set up automated payments, and used the loan to successfully manage the emergency while gradually rebuilding his credit score.

- Key Takeaway: Knowing your credit tier helps you target the right lenders, preventing rejections and keeping your financial recovery on track.

Risk Awareness: What Salaried Borrowers Must Check First

Unsecured short-term borrowing comes with real risks that every salaried professional should understand. Being aware of these challenges allows you to protect your income and financial footprint.

Understanding Key Borrowing Risks

- Credit Over-Extension Risk: Taking on a new monthly payment close to your maximum budget leaves you with very little financial flexibility. If you face further unexpected expenses the following month, you could find yourself trapped in a difficult debt cycle.

- Data Security & Privacy Risks: The digital lending market includes unverified platforms that use aggressive data collection practices. Some apps require access to your phone’s contacts, photo galleries, and location history as a condition for approval. Only work with licensed lenders that maintain strict data protection standards.

- Employment and Income Stability Risks: Your ability to pay back an unsecured loan depends entirely on your regular monthly salary. If your company faces downsizing, restructuring, or payment delays, managing an expensive loan can become incredibly difficult. Always try to keep your loan balances low relative to your income.

To manage these risks effectively, take the time to verify every lender, read the fine print, and consult a qualified financial professional for major personal finance decisions.

Checklist Before Submitting an Urgent Loan Application

Before you hit the final submit button on a loan application portal, review this quick verification checklist to ensure you are borrowing safely:

- Lender Verification: Confirmed that the lender is a regulated financial institution or an authorized bank partner.

- Credit Score Check: Pulled your latest credit report to check your score and ensure there are no reporting errors.

- Debt-to-Income Calculation: Verified that your total monthly debt payments (including the new loan) stay below 45% of your net salary.

- Document Prep: Saved original digital PDFs of your last 3 to 6 months of bank statements and your official identity proofs.

- True Cost Review: Read the formal loan summary to verify the exact interest rate, processing fees, and annual percentage rate (APR).

- Foreclosure Terms: Checked that the agreement allows you to pay off the loan early without excessive prepayment penalties.

- Budget Match: Confirmed that the new monthly payment fits comfortably into your upcoming household budgets.

- Data Safety: Verified that the application portal uses secure, encrypted connections and does not request unnecessary phone permissions.

Using this checklist before making major borrowing choices helps you stay organized, prevent rejections, and protect your personal financial health.

Strategic Insights for Long-Term Debt and Financial Planning

For professionals looking to build long-term financial security, managing short-term debt requires a clear understanding of your overall capital structure.

1. Monitoring Your Debt-to-Income Ratio

Your debt-to-income ratio is a key indicator of your financial health. A ratio below 30% shows that your debt is well-managed, giving you plenty of financial breathing room. A ratio between 30% and 45% is manageable but requires caution, while a ratio above 45% indicates that your fixed costs are too high, meaning you should avoid taking on any new debt.

2. Managing Lifestyle Inflation

As your career progresses and your salary grows, it is easy to increase your discretionary spending on premium choices. This trend, known as lifestyle inflation, can prevent you from building meaningful savings. Keeping your fixed living expenses steady as your income grows creates a natural financial cushion, protecting you from needing emergency loans in the future.

3. Creating an Automated Savings System

The most effective way to handle future emergencies is to build a dedicated personal savings fund. By setting up an automated transfer that moves 10% to 15% of your paycheck into a separate savings account on payday, you can gradually build a cash reserve. Over time, this fund can cover unexpected costs directly, freeing you from relying on high-interest emergency loans entirely.

Key Terms Explained for Beginners

- Unsecured Loan: A loan granted based solely on the borrower’s creditworthiness and income stability, without requiring any physical assets like land or gold as collateral.

- Credit Bureau: A regulated company that collects and maintains consumer credit histories, using that data to generate credit reports and scores for lenders.

- Hard Inquiry: A formal credit history check pulled by a lender when evaluating an application, which temporarily lowers your credit score by a few points.

- Annual Percentage Rate (APR): The total true cost of a loan on an annual basis, combining the base interest rate plus all mandatory processing and onboarding fees.

- Debt Consolidation: The financial strategy of taking out a single lower-interest loan to pay off multiple higher-interest debts, leaving you with just one manageable monthly payment.

- Loan Foreclosure: Paying off the entire remaining balance of a loan in a single payment before the agreed tenure ends.

- Automated Clearing House (ACH): A secure electronic network used to handle automated monthly payment deductions directly from a borrower’s checking account.

- Principal Amount: The original sum of money borrowed from a lender, not including interest charges or processing fees.

- Risk-Based Pricing: A method where lenders set loan terms and interest rates based on the applicant’s individual credit risk profile.

- Net Take-Home Pay: The actual amount of money deposited into an employee’s bank account on payday after all tax and benefit deductions.

Who Should Read This Comprehensive Guide

1. Early-Career Salaried Professionals

Young workers who are building their initial savings often face tight budgets when unexpected expenses come up. This guide provides a practical blueprint to help you understand institutional borrowing and avoid high-cost credit traps.

2. Mid-Level Corporate Staff Managing Family Finances

Professionals balancing rent, childcare, and everyday household costs benefit from understanding how lenders evaluate debt capacity. This knowledge helps you secure clean, low-cost loans when your family needs them most.

3. Loan Seekers Evaluating Quick Credit Options

Individuals actively looking for urgent financing online can use this checklist to audit their profile before applying. This ensures you target the right lenders, speed up approval times, and keep your long-term finances secure.

Frequently Asked Questions

What is an emergency loan for salaried employees?

An emergency loan is an unsecured personal loan designed to provide rapid access to capital during unexpected crises, evaluated based on your monthly salary and credit history.

Why is checking emergency loan eligibility important for beginners?

Checking your eligibility beforehand protects your credit score from excessive hard inquiries and saves critical time during a high-stress financial crisis.

How can a salaried employee start the application process safely?

Start by pulling your credit report, calculating your current debt ratio, organizing your digital financial documents, and choosing a single reputable lender that matches your profile.

What is the single biggest mistake to avoid during urgent borrowing?

The biggest mistake is applying to multiple lenders simultaneously out of panic, which signals financial distress to underwriting systems and lowers your credit score.

Is this eligibility checklist useful for professionals working at small businesses?

Yes, the core principles of evaluating your debt-to-income ratio, organizing clean bank statements, and checking your credit score apply to salaried employees at companies of all sizes.

What specific credit score do major banks require for low-interest loans?

Most major institutions look for a credit score of 750 or higher to unlock their lowest interest rates and fastest automated approval pathways.

How does a lender calculate my debt-to-income ratio?

Lenders add up all your active monthly loan payments and credit card bills, then divide that total by your net monthly take-home income to find your debt percentage.

Should I seek professional advice before taking out a short-term emergency loan?

Yes, consulting a qualified financial advisor is highly recommended if you are unsure about loan terms, face complex debt issues, or need help managing your long-term budget.

How often should a working professional review their personal credit report?

It is best practice to review your credit file at least once every quarter to spot and fix reporting errors before you face an actual borrowing emergency.

What hidden charges should I check for in the loan agreement fine print?

Always review the agreement for processing fees, documentation charges, early closure penalties, and late payment interest rates hidden within the terms.

How does a short-term emergency loan assist with overall financial planning?

When used carefully, it provides a stable bridge to handle immediate crises without forcing you to drain your long-term retirement accounts or liquidate long-term investments.

What is the best practical next step after reading this comprehensive checklist?

The best next step is to log into an authorized credit portal, pull your baseline credit score, and set up a secure digital folder for your core income documents.

Conclusion and Next Steps

Navigating an unexpected financial emergency does not have to break your long-term financial security. While a sudden medical cost, vehicle breakdown, or urgent home repair can be stressful, moving forward with a clear, organized approach is the key to managing the challenge successfully. Unsecured personal loans are effective tools for salaried employees during a crisis, provided you treat them with care and respect.

As we have covered in this guide, securing an affordable, low-cost loan depends on understanding your eligibility profile before you speak with a lender. Taking a few minutes to audit your credit score, calculate your debt-to-income ratio, and organize your original digital documents saves valuable time during an emergency. This preparation helps you avoid the common mistakes of applying to too many lenders or falling for high-interest, predatory platforms.

Once you resolve your immediate cash crunch, use the experience to build stronger financial habits for the future. Focus on keeping your monthly debt burdens low, tracking your discretionary expenses, and gradually building a dedicated personal savings fund. Having a cash reserve to handle life’s surprises is the ultimate step toward true financial freedom.

For now, take a structured approach to your current needs. Review the eligibility checklist, compare your options carefully, read the fine print, and make a logical borrowing decision that protects both your immediate needs and your future financial health.