Introduction

Life has a way of throwing unexpected financial curveballs when you least expect them. You might be cruising through your month smoothly, keeping a close eye on your monthly budget, when suddenly your car breaks down, a medical issue arises, or an urgent home repair demands immediate attention. In these moments, your regular monthly income might not cover the sudden expense, leaving you searching for quick financial assistance. This is where a small emergency loan can become a practical safety net.

When facing an unexpected financial crisis, finding a quick, reliable solution is crucial. An instant personal loan in India can provide emergency credit for salaried employees and self-employed individuals, helping bridge the gap between sudden expenses and your next paycheck. However, borrowing money should never be a hasty decision. While an online loan application makes accessing funds easier than ever, it requires careful thought and a strong sense of financial discipline.

In this comprehensive guide, we will break down everything you need to know about navigating urgent financial needs. You will discover exactly what a small emergency loan is, explore common scenarios where it makes sense to borrow, and learn how to evaluate your financial situation. We will also dive into eligibility criteria, walk through the step-by-step online application process, and share essential responsible borrowing tips to keep your finances secure. By the end of this article, you will have a clear, practical roadmap to help you decide if an urgent cash loan online is the right choice for your specific situation.

What Is a Small Emergency Loan?

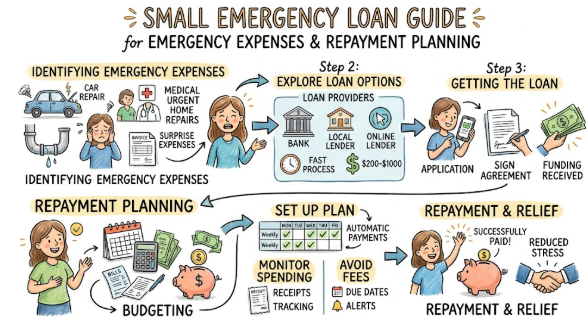

A small emergency loan is a short-term personal loan designed specifically to help individuals cover sudden, unbudgeted expenses. Unlike traditional bank loans that involve lengthy paperwork, high borrowing amounts, and weeks of processing time, these loans focus on smaller amounts and faster access. They function as a form of personal loan for urgent needs, providing a financial cushion when you face a temporary cash crunch.

In India’s evolving financial landscape, digital lending platforms and non-banking financial companies (NBFCs) have simplified this borrowing process. These financial products are typically unsecured, meaning you do not need to pledge any collateral or assets, like gold or property, to secure the funds. Instead, financial institutions evaluate your application based on your regular monthly income, employment stability, and credit history. Because the risk for lenders is higher with unsecured products, the interest rates can be higher than standard long-term loans. Therefore, these loans are best used for short-term, critical needs rather than long-term financial planning.

Common Scenarios Requiring a Small Emergency Loan

Recognizing the difference between a true financial emergency and a temporary lifestyle desire is the foundation of smart money management. A small emergency loan is an ideal tool when delaying an expense will cause greater financial or personal hardship. Here are the most common, legitimate situations where opting for an urgent cash loan online may be justified:

- Sudden Medical Expenses: Medical emergencies are unpredictable and often expensive. Even if you have health insurance, certain costs like specific medicines, diagnostic tests, or initial hospital deposits might require immediate out-of-pocket payment. An instant personal loan in India can help cover these sudden medical bills without disrupting your long-term savings.

- Urgent Vehicle Repairs: For many working professionals, a car or two-wheeler is essential for daily commuting. If your vehicle breaks down unexpectedly, fixing it immediately is vital to maintaining your livelihood. A short-term cash loan can cover the repair costs, ensuring you don’t miss work or lose daily wages.

- Essential Home Repairs: Severe plumbing leaks, electrical faults, or structural damage during the monsoon season require immediate attention. Delaying these repairs can worsen the damage and lead to significantly higher expenses later. Utilizing emergency financial help to resolve these issues early can protect both your home and your wallet.

- Critical Tech or Work Tool Replacements: If you are a freelancer, remote worker, or IT professional, your laptop or computer is your primary source of income. A sudden hardware failure can bring your work to a complete standstill. Getting a small emergency loan to replace or repair your work equipment ensures you keep earning without major interruptions.

- Unplanned Family Commitments: Sometimes, you may need to travel at short notice due to a family crisis or an urgent domestic obligation. Last-minute train or flight bookings can be expensive, and a quick personal loan can help manage these travel costs during a sensitive time.

Small Emergency Loan Eligibility and Documents

Before initiating an online loan application, it is important to understand what lenders look for during the evaluation process. Every financial institution maintains specific criteria to determine your creditworthiness and repayment capacity. Being aware of these requirements beforehand can help you prepare your paperwork and streamline your approval process.

The table below outlines the core components of emergency loan eligibility and details why each factor matters to financial institutions:

Small Emergency Loan Eligibility and Documents Table

| Eligibility/Requirement | What It Means | Why It Matters |

| Age | Must meet lender’s age criteria | Basic eligibility check |

| Income Proof | Salary slips, bank statements | Confirms repayment ability |

| Employment Type | Salaried or self-employed | Stability check |

| Credit Score | History of repayments | May impact approval & rate |

| KYC Documents | PAN, Aadhaar, address proof | Legal compliance |

| Bank Account | Active account | Essential for processing |

How to Decide If You Truly Need a Loan

When an unexpected expense arrives, it is easy to panic and rush into borrowing. However, taking a moment to step back and assess the situation objectively can save you from unnecessary debt. Ask yourself a few critical questions before submitting an online application. Is this expense absolutely essential right now, or can it wait until your next salary cycle? For instance, buying a new smartphone because your current one has a minor scratch is a luxury; replacing a phone that is completely broken and essential for your daily work is a necessity.

Next, take a look at your available resources. Check if you can cover the cost by adjusting your current month’s variable spending, such as cutting back on dining out, entertainment, or shopping. If the amount required is relatively small, you might be able to handle it by pulling minor amounts from different areas of your budget. Borrowing should always be your last line of defense, reserved for situations where you have exhausted your immediate cash flow options and the expense cannot be postponed.

Pros and Cons of Small Emergency Loans

Every financial product comes with its own set of advantages and drawbacks. Evaluating both sides of the coin will help you make a balanced, well-informed financial decision.

The Advantages (Pros)

- Quick Processing and Convenience: The digital nature of modern micro-loans means you can apply from the comfort of your home or office, avoiding lengthy bank visits.

- Minimal Documentation: Unlike traditional loans that demand extensive paperwork, small loans usually require basic KYC and income verification documents.

- No Collateral Required: Because these are unsecured loans, you don’t have to risk personal assets to secure financial assistance.

- Flexible Repayment Options: Most lenders offer short-term repayment windows, allowing you to pay off the debt quickly within a few months and move on.

The Disadvantages (Cons)

- Higher Interest Rates: Due to the unsecured nature and rapid processing, these loans often carry higher interest rates compared to standard long-term loans.

- Impact on Credit Score: If you miss an Equated Monthly Installment (EMI) or delay a payment, your credit score will drop, making future borrowing more difficult.

- Risk of Debt Traps: The ease of accessing online cash can tempt some individuals to borrow repeatedly, leading to a cycle of high-interest debt.

- Processing Fees and Penalties: Lenders usually charge upfront processing fees, and late payments attract hefty penalty charges that can add up quickly.

Step-by-Step Online Application Process

If you have evaluated your options and decided that a small personal loan is necessary, the online application process is straightforward. Here is a typical walkthrough of how to navigate your application successfully:

[Choose a Lender] ➔ [Select Amount & Tenure] ➔ [Fill Details & Upload KYC] ➔ [Verification] ➔ [Disbursal]

- Research and Compare Lenders: Start by visiting credible financial platforms to compare interest rates, processing fees, and repayment terms. Look for recognized, RBI-registered NBFCs or banks to ensure your data and transactions remain secure.

- Select Your Loan Amount and Tenure: Use an online EMI calculator to input the exact amount you need. Adjust the repayment tenure (usually ranging from 3 to 12 months) to find an EMI amount that fits comfortably into your monthly budget without straining your regular expenses.

- Fill Out the Digital Application: Provide your basic personal information, including your full name, mobile number, email address, and employment details. Double-check all entries for accuracy, as minor typographical errors can lead to delays or immediate rejection.

- Upload Required Documents: Upload scanned copies or clear photos of your primary documents. This typically includes your PAN card, Aadhaar card, recent salary slips, and updated bank account statements showing your regular income flow.

- Await Verification and Approval: The lender’s automated system, along with their underwriting team, will assess your credit profile, verify your employment details, and run a quick credit check. This stage determines your final interest rate and approved loan amount.

- Accept the Loan Terms and Receive Disbursal: Once approved, you will receive a digital loan agreement outlining the interest rate, processing fees, and repayment schedule. Read the terms and conditions carefully. If you agree, sign the document electronically; the funds are typically transferred directly into your verified bank account shortly after.

Real-Life Example: Managing an Unplanned Expense

To better understand how this works in practice, let’s look at a realistic scenario involving Rajesh, a 28-year-old software analyst working in Bengaluru.

Rajesh earns a net monthly salary of ₹45,000. He manages his money well, allocating funds for rent, groceries, utilities, and a small mutual fund SIP. However, midway through the month, his refrigerator stops working completely. The technician informs him that a vital component has failed, and repairing it will cost ₹12,000. Since it’s mid-summer, a refrigerator is an absolute necessity to prevent food from spoiling.

Rajesh checks his savings account and realizes he only has ₹4,000 left after paying his regular bills, leaving him ₹8,000 short. He decides against asking friends for money and opts to look for an instant personal loan in India.

How Rajesh Handled It Responsibly:

- Borrowed Only What Was Needed: Although the lending app offered him a credit limit of ₹25,000, Rajesh chose to borrow exactly ₹8,000 to cover the repair cost.

- Selected a Short Tenure: He chose a comfortable 3-month repayment tenure, making his monthly EMI roughly ₹2,800.

- Adjusted His Monthly Budget: To accommodate this new ₹2,800 monthly expense for the next three months, Rajesh decided to cut back on weekend food deliveries and OTT entertainment subscriptions.

Because Rajesh maintained a disciplined approach, he resolved his urgent household crisis quickly without slipping into long-term financial trouble. He paid his EMIs on time, which also helped maintain his healthy credit history.

Key Factors to Check Before Applying

Before you click the final “Submit” button on any loan application, it is essential to look past the attractive marketing headlines. Focus on the core numbers that determine the actual cost of your loan.

First, examine the Annual Percentage Rate (APR), which represents the total cost of borrowing over a year, including the base interest rate and any mandatory processing fees. Sometimes a loan may seem to have a low interest rate, but hidden processing fees or administrative charges can make it more expensive overall. Always read the fine print regarding prepayment or foreclosure charges; some lenders charge extra fees if you try to pay off your loan early, while others encourage it. Knowing these terms in advance helps prevent unpleasant surprises on your financial statements later.

Risks and Limitations of Short-Term Borrowing

While an urgent cash loan online offers immediate financial relief, it is important to remember that it is a serious financial commitment. Borrowing money brings specific risks that can impact your overall financial well-being if not managed with care.

The most immediate risk is the financial pressure a new monthly EMI adds to your budget. If your income is already stretched thin, introducing a fixed repayment obligation can make it harder to pay for essential needs like rent, groceries, and utilities. Missing an EMI payment can result in high late fees and penalty interest charges that compound rapidly, causing a small initial balance to grow quickly. Furthermore, defaults or late payments are reported to credit bureaus like CIBIL, lowering your credit score and making it more difficult to secure crucial financing, such as home or car loans, in the future.

Emergency Loan Consideration Checklist

Before moving forward with a loan application, take a moment to review your readiness. Walking through a structured checklist can clarify your choice and ensure you are borrowing for the right reasons.

The table below serves as a practical assessment tool to verify if you have covered all critical aspects of responsible borrowing:

Emergency Loan Consideration Checklist Table

| Checklist Point | Status |

| Financial need genuine | Yes/No |

| Loan amount calculated | Yes/No |

| EMI affordability checked | Yes/No |

| Interest rate compared | Yes/No |

| Processing fee reviewed | Yes/No |

| Documents ready | Yes/No |

| Lender credibility verified | Yes/No |

| Terms & conditions reviewed | Yes/No |

| Repayment date noted | Yes/No |

| Backup emergency funds considered | Yes/No |

Common Mistakes to Avoid

When looking for emergency credit for salaried employees, minor oversights can lead to financial stress. Being aware of common pitfalls can help you navigate the process safely:

- Borrowing More Than Necessary: When a lender approves you for a high credit limit, it can be tempting to take the full amount and use the extra cash for shopping or dining out. Remember, you have to pay interest on every single rupee you borrow. Stick strictly to the exact amount required to resolve your immediate emergency.

- Ignoring the Fine Print: Rushing through an application without reading the terms and conditions can lead to unexpected costs later. Pay close attention to hidden fees, bounce charges, late payment penalties, and foreclosure terms before signing the digital contract.

- Applying with Multiple Lenders Simultaneously: When you submit applications to several lenders at the same time, each lender runs a hard inquiry on your credit profile. Multiple hard inquiries within a short period can signal financial distress to credit bureaus, causing your credit score to drop.

- Overestimating Your Repayment Capacity: Assuming you will easily pay off a loan without reviewing your actual cash flow can lead to missed payments. Always look at your real take-home salary and current fixed commitments before agreeing to a new monthly EMI.

Practical Tips for Responsible Borrowing

If you decide to move forward with a small emergency loan, practicing good financial discipline will ensure the experience remains smooth and stress-free.

First, make it a priority to automate your monthly repayments. Setting up an e-NACH mandate or auto-debit feature with your bank allows the EMI to be deducted automatically on a specific date each month, ideally right after your payday. This ensures you never miss a deadline due to forgetfulness and helps you avoid costly late fees.

Second, treat your loan as an absolute priority over non-essential lifestyle expenses. While paying off your loan, consider cutting back on discretionary spending like dining at expensive restaurants, weekend getaways, or luxury purchases. If you receive an unexpected bonus, cash gift, or freelance payment, consider using those extra funds to clear your loan ahead of schedule. Paying off your debt early reduces the total interest you pay and clears your financial plate sooner.

Alternatives to Small Emergency Loans

Taking out a personal loan is not the only way to manage a sudden cash crunch. Before committing to a new loan, consider these alternative paths that might be more cost-effective:

- Utilizing a Dedicated Emergency Fund: The most effective alternative to borrowing is having a personal emergency fund. Financial experts recommend saving three to six months’ worth of essential living expenses in a liquid savings account or fixed deposit. This fund allows you to handle unexpected expenses easily without taking on high-interest debt.

- Borrowing from Trusted Family or Friends: If you have a strong relationship with family members or close friends, consider asking for a short-term loan. This approach can help you avoid high interest rates and formal processing fees. To maintain trust, treat the arrangement professionally by setting clear terms and a firm repayment date.

- Salary Advance from Your Employer: Many companies offer an advance salary option for employees dealing with genuine medical or family emergencies. This allows you to access a portion of your upcoming paycheck early, usually with minimal administrative fees and no interest charges.

- Liquidating Small Non-Essential Investments: Look through your financial portfolio to see if you have short-term mutual funds, redundant fixed deposits, or gold assets that can be liquidated. Using your own accumulated wealth to cover a crisis is often more practical than taking on new high-interest debt liabilities.

When Not to Take a Small Emergency Loan

There are times when borrowing money can worsen a financial situation rather than helping it. Recognizing these warning signs can help protect you from falling into a deeper debt trap.

Never take out an emergency loan to fund luxury lifestyle choices, such as buying premium gadgets, funding a vacation, or hosting an expensive party. These are discretionary expenses that should be funded through patient monthly saving, not high-interest credit. Additionally, avoid using a new personal loan to pay off existing credit card debt or other micro-loans. Using credit to clear credit creates a dangerous cycle of compounding debt that can severely damage your long-term financial health. If you are already struggling to pay for basic necessities like rent or groceries, taking on more interest-bearing debt is rarely a sustainable solution. In those situations, focusing on budgeting, cutting expenses, or seeking structural financial counseling is a safer path forward.

Frequently Asked Questions (FAQs)

Q1: How fast can I get a small emergency loan online?

A1: Disbursal times vary depending on the lender’s policies and your individual profile. Many modern digital platforms can process and transfer funds within a few hours of document verification, while traditional institutions might take one to two business days.

Q2: Will applying for an emergency financial help loan affect my credit score?

A2: Yes, the initial application triggers a hard inquiry, which may cause a minor, temporary dip in your credit score. Moving forward, making your EMI payments consistently on time can help build and strengthen your long-term credit history.

Q3: Can I apply for a small loan if I am a freelancer or self-employed?

A3: Yes, many digital lenders offer short-term cash loans to self-employed individuals and freelancers. You will typically need to provide steady proof of income, such as income tax returns (ITR) and detailed bank account statements from recent months.

Q4: What happens if I miss an EMI payment on my instant personal loan?

A4: Missing an EMI payment usually results in substantial late fees and penalty interest charges from your lender. Additionally, the default is reported to credit bureaus, which will lower your credit score and make future borrowing more challenging.

Q5: Are there any hidden charges I should look out for during an online loan application?

A5: While reputable lenders list their fees clearly, always review the loan agreement for processing fees, documentation charges, technology platform fees, e-mandate bounce charges, and loan foreclosure penalties.

Q6: Can I pay off my small emergency loan early before the tenure ends?

A6: Most lenders allow early repayment or foreclosure, but policies vary. Some institutions let you pay off the balance with zero penalties after a certain number of months, while others may charge a minor prepayment fee. Always check these terms beforehand.

Q7: What is the minimum credit score required for emergency credit for salaried employees?

A7: While a credit score of 750 or above is ideal for securing favorable interest rates, many fintech platforms consider profiles with lower scores or limited credit history, though this often comes with higher interest rates to offset the risk.

Q8: Can I get an emergency loan without income proof?

A8: It is very difficult to secure an unsecured emergency loan without showing a steady source of income. Lenders need verification, such as salary slips or bank statements, to ensure you have the financial capacity to repay the borrowed amount.

Q9: How do I verify if an online loan app is real and safe?

A9: Always check if the platform is partnered with an RBI-registered bank or NBFC. Avoid apps that demand upfront processing fees before approving your loan, or those that don’t clearly state their physical address and customer support details.

Q10: Is it better to use a credit card or a small emergency loan for urgent needs?

A10: If you can pay off your credit card balance in full during the next billing cycle, a credit card can be a cost-effective choice due to its interest-free period. However, if you need multiple months to repay the amount, a small personal loan often offers lower interest rates than standard credit card revolving interest.

Conclusion

A small emergency loan can be an effective and reliable tool to navigate sudden financial challenges when used thoughtfully. Whether you are dealing with a medical emergency, unexpected vehicle repairs, or an urgent tool replacement, an instant personal loan in India can provide timely support when traditional channels take too long.

However, the key to successful borrowing lies in strict financial discipline and careful planning. Always remember to borrow only what you truly need, compare multiple offers to find competitive interest rates, and ensure your upcoming monthly EMIs fit comfortably within your take-home pay. By treating debt as a deliberate commitment and maintaining a strong repayment track record, you protect your credit health and build a stronger financial future.