Introduction

Life has a unique way of throwing curveballs when you least expect them. You might be sailing smoothly through the month, tracking your expenses diligently, when suddenly, an unexpected medical bill lands in your lap, or your car breaks down in the middle of a busy work week. Suddenly, you are facing an emergency cash crisis.

When a financial emergency strikes, it is incredibly easy to panic. Your heart rate spikes, stress levels soar, and you might feel tempted to opt for the very first financial solution you find, even if it carries exorbitant interest rates or predatory terms. However, navigating a sudden financial shortfall requires a calm mind and a strategic approach. Navigating an emergency cash crisis smoothly comes down to having access to the right information and knowing what steps to take.

In this comprehensive guide, we will break down actionable, beginner-friendly personal finance tips and emergency cash solutions tailored specifically for Indian salaried professionals, freelancers, and families. Whether you are dealing with a temporary salary delay or an unforeseen domestic expense, this guide will empower you with the tools needed for effective short-term financial management and responsible borrowing.

Understanding Emergency Cash Crises

An emergency cash crisis occurs when you face an immediate, unavoidable expense that cannot wait until your next payday, and your readily available bank balance is insufficient to cover it. It is crucial to understand that a cash crisis is fundamentally a liquidity problem, not a reflection of your long-term financial worth.

Many people confuse a cash crisis with general poverty or long-term debt traps. However, even individuals with good salaries can find themselves in need of urgent money help due to poor asset allocation or bad timing. For example, if most of your money is locked up in fixed deposits, mutual funds, or real estate, you might struggle to find immediate liquid cash when an emergency hits. Therefore, learning how to manage these short-term gaps without disrupting your long-term financial health is an essential life skill.

Common Scenarios Leading to Cash Shortages

Unplanned expenses come in many shapes and sizes. Recognizing these scenarios can help you prepare mentally and structurally for handling unexpected expenses before they spiral out of control.

- Sudden Medical Expenses: Even if you have health insurance, certain hospital charges, diagnostic tests, or specialized medicines require upfront out-of-pocket payments. Because medical situations are time-sensitive, they represent the most common cause of sudden cash crunches.

- Salary Delays: For salaried professionals and freelancers alike, a delay in payment processing from an employer or client can completely throw off a monthly budget. Implementing salary delay tips, such as keeping a minor cash buffer, can help mitigate this specific issue.

- Urgent Utility and Maintenance Bills: Missing a crucial electricity bill, society maintenance charge, or insurance premium can lead to penalties or service disconnections.

- Critical Vehicle or Home Repairs: A broken gearbox in your car or a major plumbing leak at home cannot wait. Because you rely on these assets daily, repairing them becomes an absolute priority.

- Family and Social Emergencies: Sometimes, a family member might need immediate financial assistance due to an unexpected setback, requiring you to send money home instantly.

- Unexpected Education Fees: Mid-term school excursions, sudden lab fees, or unplanned textbook purchases can catch parents off guard, forcing them into fast urgent cash planning.

Emergency Loan Eligibility & Documents

| Requirement | What It Means | Why It Matters |

| Age | Must meet the lender’s specific age criteria (typically between 21 and 60 years old). | Serves as a basic legal and eligibility check to ensure the borrower is of legal working age. |

| Income Proof | Submission of recent salary slips, Form 16, or official bank statements. | Confirms your steady repayment ability and helps the lender calculate your debt-to-income ratio. |

| Employment Type | Status as a full-time salaried employee, registered freelancer, or self-employed individual. | Acts as a stability check; lenders prefer a consistent history of employment or business revenue. |

| Credit Score | Your historical repayment track record, typically pulled from CIBIL or Experian. | May significantly impact your loan approval odds, processing speed, and assigned interest rate. |

| KYC Documents | Officially valid identity and address verifications, such as your PAN and Aadhaar. | Ensures absolute legal compliance with Reserve Bank of India (RBI) anti-money laundering guidelines. |

| Bank Account | A functional, active savings account with internet banking or debit card access enabled. | Required for seamlessly processing and disbursing funds, as well as setting up automated repayments. |

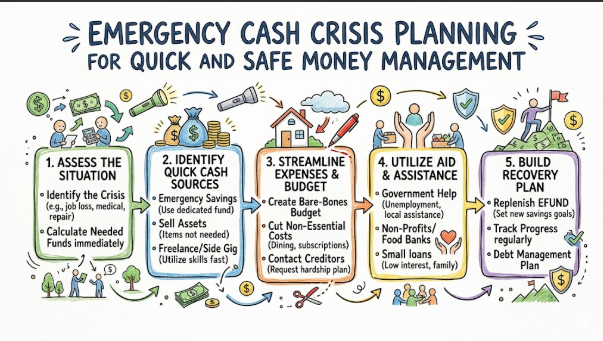

Smart Ways to Handle a Cash Crisis

If you find yourself in a tight spot today, do not panic. Take a structured approach by focusing on these core cash shortage solutions:

- Review Your Emergency Savings First: Before looking outward for loans, check if you have any micro-savings, digital wallet balances, or fixed deposits that can be broken prematurely. Even a small liquid reserve reduces the total amount you need to borrow.

- Prioritize Essential Payments: Separate your expenses into “survival needs” (food, medicine, shelter) and “wants” (subscriptions, dining out, shopping). Pause all discretionary spending immediately until your cash flow stabilizes.

- Negotiate Bills or Payment Dates: Many utility providers, landlords, and service providers are willing to extend your payment due date by a week or two if you communicate with them transparently. Always ask before assuming a deadline is written in stone.

- Use Small Emergency Loans Responsibly: If borrowing is unavoidable, choose regulated non-banking financial companies (NBFCs) or banks. Avoid unregulated loan apps that promise unrealistic terms but harvest your personal data.

- Borrow Only What Is Absolutely Necessary: If your emergency expense is ₹15,000, do not borrow ₹30,000 just because you qualify for it. Every extra rupee borrowed incurs interest and adds unnecessary pressure to your future income.

- Track Your Repayments Carefully: The moment you take out a short-term loan, mark the EMI due dates on your digital calendar. Setting up auto-debit features ensures you never hurt your credit score through a missed payment.

Step-by-Step Online Emergency Loan Application

Applying for a digital emergency loan in India has become highly streamlined, but doing it correctly saves time and protects your financial profile. Follow these clear steps:

- Select a Credible Lender: Research platforms verified by the RBI. Look for transparent fee structures and positive user reviews on official app stores.

- Check Your Base Eligibility: Use online eligibility calculators to see if your monthly income matches the lender’s threshold without leaving a hard inquiry on your credit report.

- Gather Your Information: Keep soft copies of your PAN, Aadhaar, past 3 months’ bank statements, and company ID card ready on your device.

- Fill Out the Online Application: Complete the personal, professional, and financial fields carefully. Double-check for typos in your name or account numbers, as errors can trigger automated rejections.

- Complete Digital KYC: Perform the video-KYC or Aadhaar-based OTP verification as requested by the secure portal.

- Review the Loan Terms Thoroughly: Pay close attention to the Annual Percentage Rate (APR), processing fees, pre-closure charges, and late penalty terms.

- Accept and Sign the Agreement: If the interest rates and monthly EMIs are affordable and fit your budget, digitally sign the loan agreement using an e-sign OTP.

- Wait for Disbursal: Once approved, funds are usually transferred directly to your verified bank account via IMPS or NEFT within a few hours.

Practical Tips for Managing Cash Shortages

When physical cash or liquid bank balances run low, minor adjustments to your daily routine can act as a financial cushion.

- Cut Discretionary Spending Instantly: Temporarily delete food delivery and entertainment apps from your phone. Preparing meals at home using existing pantry supplies can save thousands of rupees over a two-week period.

- Leverage Digital Wallets and Pay-Later Features Wisely: If you have pre-approved, interest-free buy-now-pay-later (BNPL) balances for grocery purchases, use them to preserve your physical cash for non-negotiable cash-only expenses. However, ensure you pay these off during the next billing cycle.

- Track Every Single Micro-Expense: Use a simple notebook or a smartphone app to log every rupee spent, from a quick cup of tea to commuting costs. Increased visibility naturally curbs impulsive outlays.

- Create a Temporary “Survival Budget”: Draft a bare-bones 14-day or 30-day budget plan that covers only the absolute essentials required to keep your household functioning until your next influx of income.

- Consolidate Urgent Payments: If multiple small bills are due simultaneously, use your remaining cash to settle the ones that carry heavy late fees or immediate service cutoff threats, while deferring more lenient obligations.

Real-Life Example: Navigating a Cash Crunch

Let’s look at a relatable example to see how these principles apply in the real world.

Meet Rahul, a 28-year-old UX designer living in Hyderabad. Rahul earns a comfortable salary, but due to a sudden technical transition at his firm, his monthly salary disbursement was delayed by twelve days. To make matters worse, his refrigerator broke down during the exact same week, spoiling his groceries and requiring an immediate repair cost of ₹8,000. Additionally, his grandmother’s monthly pharmacy bill of ₹4,500 was due.

Instead of panicking or turning to unverified peer-to-peer lenders online, Rahul took a systematic approach:

- He reviewed his bank balances and pulled together ₹5,000 from a digital wallet buffer he had forgotten about.

- He communicated with his landlord, explaining the formal salary delay company notice. Because of his excellent past track record, the landlord happily extended his rent due date by two weeks without any penalty.

- To bridge the remaining gap for the refrigerator repair and medicines, Rahul applied for a small emergency loan of ₹10,000 through a trusted digital platform.

- Because his KYC documents were up to date, the money was disbursed within four hours.

Rahul resolved his immediate crisis safely, paid for the repairs and medicine, and closed the loan entirely the moment his salary was credited twelve days later. By combining proactive communication, personal buffers, and a regulated short-term borrowing solution, he protected both his household and his long-term credit health.

Cash Crisis Handling Checklist

| Checklist Point | Description & Action Item | Current Status (Yes / No) |

| Emergency Need Verified | Have you confirmed that this expense is an absolute, unavoidable emergency and not an impulsive lifestyle luxury? | No |

| Essential Payments Prioritized | Have you safely set aside or allocated funds for your core survival expenses like food, basic utilities, and medicine? | No |

| Loan Eligibility Checked | Have you reviewed the lender’s basic criteria (income, age, location) before initiating a formal application? | No |

| Documents Ready | Are your digital copies of your PAN, address proof, and recent bank statements compiled and easily accessible? | No |

| EMI Affordability Calculated | Have you mapped out your upcoming monthly income to confirm you can easily pay off the loan without hurting future stability? | No |

| Lender Credibility Verified | Have you checked that the platform or bank is fully recognized and compliant with RBI regulations? | No |

| Terms & Conditions Reviewed | Have you explicitly read through the fine print regarding processing fees, interest rates, and potential late penalties? | No |

| Payment Schedule Planned | Is there a definitive calendar reminder or auto-debit set up to prevent accidental defaults or delayed payments? | No |

| Alternative Funds Considered | Have you exhausted options like friendly personal loans, corporate salary advances, or liquidation of micro-savings? | No |

| Monthly Review Completed | Have you committed to conducting a post-crisis evaluation of your budget to prevent similar liquid crunches next month? | No |

Common Mistakes to Avoid During a Financial Crunch

When searching for urgent money help, stepping into common financial traps can compound your problems. Avoid these mistakes:

- Borrowing More Than Your Repayment Capacity: Getting approved for a larger loan amount feels like a relief, but a larger loan means larger EMIs. Never borrow an amount that consumes more than 40% of your typical monthly take-home pay.

- Ignoring the True Cost of the Loan: Always look beyond the principal amount. Factor in processing charges, document verification fees, and insurance costs, which can quietly diminish the actual amount hitting your account.

- Falling for Unverified, Non-RBI Regulated Apps: Do not download random lending applications from unverified links or social media advertisements. These platforms often engage in unethical recovery tactics and charge usurious daily interest rates.

- Using Emergency Funds for Lifestyle Desires: If you must dip into savings or take a short-term advance, ensure the capital goes strictly toward resolving the emergency. Buying an electronics upgrade or booking a vacation during a cash shortage is a recipe for long-term debt.

- Procrastinating on Your Repayment Dates: Assuming that missing a payment by a few days “doesn’t matter” is a critical mistake. Late payments trigger immediate penalty charges and leave a lasting negative mark on your CIBIL score, making future borrowing significantly harder and more expensive.

Frequently Asked Questions

1. Who is eligible to apply for a small emergency loan in India?

Most registered financial institutions require you to be a resident citizen of India between the ages of 21 and 60. You must have a predictable, steady source of monthly income—either as a full-time salaried professional at a registered enterprise or as a self-employed individual with valid business banking credentials.

2. What are the essential documents needed for an urgent cash loan?

You generally need your Primary Identity Proof (PAN card), Address Verification (Aadhaar, Passport, or recent utility bills), and verified proof of regular income (such as your latest 3 to 6 months’ bank account statements showing salary credits, along with recent salary slips).

3. How fast can I expect emergency funds to hit my bank account?

Thanks to modern digital infrastructure, online platforms can complete automated verification very quickly. Once your digital KYC is fully authorized, the loan agreement is e-signed, and your bank account is validated, funds are frequently disbursed within a few hours.

4. Will applying for an emergency loan impact my CIBIL credit score?

Checking your preliminary pre-approved offers usually involves a “soft pull” on your credit history, which does not impact your score. However, when you formally submit a completed loan application, the lender performs a formal “hard inquiry,” which can temporarily lower your credit score by a few points. Consistent, timely repayments will ultimately boost your credit score over time.

5. What are the typical interest rates for short-term emergency cash solutions?

Interest rates fluctuate based on your underlying credit profile, income bracket, chosen lender, and repayment term. Because these are unsecured short-term personal lines of credit, annual percentage rates (APRs) can range anywhere from 12% to 36%. Always check the explicit rate offered to you before signing.

6. Are digital lending platforms entirely safe to use?

Digital lending is highly secure provided you use platforms that operate in direct, transparent partnership with RBI-registered Banks or Non-Banking Financial Companies (NBFCs). Always verify a platform’s credentials on their official website, read user feedback, and avoid apps that demand upfront processing fees before loan approval.

7. What alternatives should I check before taking an emergency loan?

Before taking out an interest-bearing loan, explore interest-free options. Check if you can get a temporary salary advance from your employer, secure a zero-interest personal loan from immediate family members, or prematurely liquidate a portion of your low-yield recurring deposits or mutual funds.

8. How do I calculate the ideal emergency loan amount for my situation?

Your loan amount should strictly match the exact cost of resolving your immediate emergency minus any liquid funds you already possess. Avoid rounding up the loan amount for extra padding, as you will pay unnecessary interest on money you don’t actively need.

9. What should salaried employees do if their pay is delayed by several weeks?

If your salary is delayed, immediately construct a minimal survival budget and map out your non-negotiable expenses. Proactively communicate with your landlord and utility providers to request grace periods. If you must borrow to bridge the gap, ensure the loan tenure is short and plan to clear the balance as soon as your salary arrives.

10. When should I consider seeking professional personal finance advice?

If you find yourself facing an emergency cash crisis almost every single month, it indicates an underlying structural issue with your cash flow or debt management. In such cases, seeking guidance from a certified financial planner can help you build an effective emergency fund and break the cycle of short-term borrowing.

Conclusion

Experiencing an emergency cash crisis can be incredibly stressful, but it is a manageable hurdle when approached with clear information and structured planning. Remember that solutions will always vary based on your specific income level, your credit history, and the lenders you choose. The absolute golden rule of navigating any sudden financial shock is to maintain clear communication with creditors, keep your documentation organized, and always practice responsible borrowing.

Temporary cash crunches can serve as powerful learning moments. Once your immediate situation settles, use the experience to jumpstart a dedicated emergency fund—even saving just ₹1,000 a month can build a meaningful safety net over time.

If you want to deepen your financial literacy, discover practical budgeting frameworks, or explore comprehensive guides on intelligent cash flow management, we are here to support your journey.