Introduction

You look at your bank account balance, and a familiar sense of dread washes over you. The numbers are dangerously close to single digits, yet your next paycheck is still a week away. This is the notorious “month-end crunch”—a financial phenomenon that affects millions of salaried professionals, freelancers, and families across India. Managing your budget perfectly for the first three weeks is a great achievement, but when the final stretch arrives, cash flow management can suddenly fall apart. The psychological weight of watching your balance dwindle while staring down unavoidable obligations can cause immense financial stress.

However, running low on cash at the end of the month does not mean you have failed financially; it often simply means your financial timing is out of sync. This is where modern financial tools come into play. Understanding how short-term loans help during month-end money problems can transform a stressful week into a manageable minor transition. Instead of dipping into long-term investments or asking friends for awkward favors, these specialized credit options bridge the gap safely when used responsibly.

The final week of the month frequently brings a unique combination of financial challenges that can disrupt even the most disciplined budgeters. Here is a summary of why those final days can feel so difficult:

- Unexpected and Unpredictable Expenses: From sudden vehicle repairs on your daily commute to a last-minute medical prescription, emergencies do not check your calendar before arriving.

- Systemic Salary Delays: When the end of the month falls on a weekend or a bank holiday, your paycheck might arrive a few days late, throwing off your entire payment schedule.

- Overlapping Urgent Bills: Internet dues, utility bills, maintenance fees, and school fees often carry strict month-end deadlines with heavy late fees if missed.

- The Rent and EMI Cycle: Landlords and home loan providers expect their money precisely on the 1st, meaning you need a secure pool of cash ready before your new salary actually clears.

What It Is

A short-term loan is a small, unsecured personal loan specifically structured to bridge temporary financial gaps. Unlike traditional bank loans that involve massive amounts, long repayment tenures, and weeks of paperwork, these are nimble financial instruments. They typically offer smaller loan values tailored for salaried employees and are designed to be paid back quickly—often within a few weeks to a few months—as soon as your next regular income arrives. Think of them as a modern, digital version of a salary advance loan.

Why It Matters

When you are caught in a temporary cash crunch, time is of the essence. Understanding how short-term loans help during month-end money problems matters because it gives you a controlled, predictable way to maintain cash flow management without destabilizing your life.

- Prevents Late Fees: It allows you to pay credit card bills and utilities on time, protecting you from compounding penalty charges.

- Avoids Financial Stress: Knowing you can cover an emergency cash loans requirement instantly eliminates the sleepless nights associated with liquidity shortfalls.

- Protects Your Credit Score: Missing an EMI or credit card payment can damage your credit profile for years; an instant personal loans solution ensures your record remains spotless.

- Preserves Long-Term Savings: You won’t have to break a fixed deposit (FD) or liquidate mutual funds early, keeping your future wealth-building goals completely intact.

Why Month-End Cash Shortages Happen

To solve a problem permanently, we must first understand its root causes. Month-end cash shortages rarely happen because of a single bad decision; rather, they are usually the result of a combination of overlapping structural and behavioral factors.

[Income Input] ──► (Fixed Commitments / Rent / EMIs) ──► (Daily Lifestyle / Variable Spending) ──► [Unexpected Month-End Emergency] ──► Cash Crunch

Moreover, the modern Indian economy moves incredibly fast. With UPI making spending effortless, it is easier than ever to lose track of minor transactions until they add up to a significant amount by week four.

- Poor Initial Planning and Budgeting: Many individuals follow a “spend first, save what’s left” philosophy. Without allocating funds for basic variable expenses early in the month, the remaining balance evaporates long before the next payday.

- The Assault of Unexpected Expenses: No matter how well you plan, life happens. A broken smartphone screen, a sudden plumbing leak at home, or an invitation to an unplanned family event can easily drain a fragile cash reserve.

- Delayed Salary Disbursal: For freelancers and contractors, payment cycles are notoriously erratic. Even for corporate employees, accounting delays or corporate transitions can occasionally push payday back by three to five crucial days.

- Clustered Recurring Bills: Many service providers intentionally align their billing cycles with the calendar month-end. When your electricity, broadband, gym membership, and insurance premiums hit your account simultaneously, your liquidity takes a massive blow.

- The Psychology of Impulse Spending: It is highly common to overspend during the first week of the month when your bank balance looks abundant. This initial lifestyle inflation directly creates a painful deficit during the final seven days.

Short-Term Loan Eligibility & Documents

| Requirement | What It Means | Why It Matters |

| Age | Must meet the lender’s specific age criteria (typically between 21 and 58 years old). | Ensures legal borrowing eligibility and confirms the applicant is within active working years. |

| Income Proof | Recent salary slips (usually past 3 months) and updated bank statements. | Confirms your steady repayment ability and helps determine the safe loan amount you can handle. |

| Employment Type | Active employment as a salaried professional or a verified, regular income stream as a self-employed freelancer. | Serves as a stability check for the lender to ensure the loan can be closed on schedule. |

| Credit Score | Your past repayment history tracks compiled by bureaus like CIBIL. | While short-term loans are more accessible, a healthy score can secure better interest rates and faster approvals. |

| KYC Documents | Standard government identity papers including PAN and Aadhaar, along with valid address proof. | Mandatory for legal regulatory compliance under RBI guidelines to prevent identity fraud. |

| Bank Account | A functional, active savings bank account with net banking capabilities enabled. | Required for the instant digital disbursal of funds and setting up automated, hassle-free repayments. |

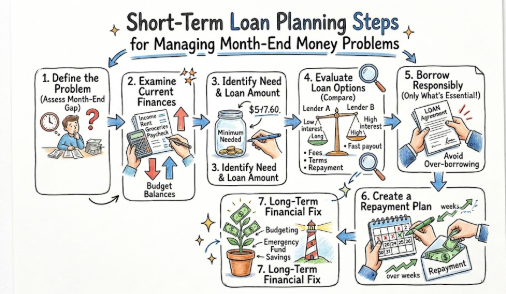

Step-by-Step Guide to Applying for Short-Term Loans

If you have decided that an emergency cash loans option is the right path for your situation, navigating the digital application process is straightforward. Here is exactly how to do it efficiently:

- Check Your Personal Eligibility StatusBefore reaching out to any provider, review your numbers. Ensure you meet the minimum income requirements and age thresholds set by modern digital platforms to prevent unnecessary application rejections.

- Choose a Reliable Lender or PlatformResearch platforms like EBORROW.IN that prioritize transparency. Look for recognized non-banking financial companies (NBFCs) or registered fintech entities to ensure you are dealing with a secure, lawful partner.

- Prepare Your Required Documents in AdvanceGather your digital files. Having your PAN, Aadhaar, recent salary slips, and past three months’ bank account statements downloaded as PDFs saves valuable time during the upload phase.

- Submit Your Application Fully OnlineFill out the digital application form accurately. Avoid typos in your name, income details, or employer information, as minor errors can trigger automated system flags and delay your salary gap solutions.

- Review the Terms, Interest Rates, and Processing FeesOnce pre-approved, read the fine print carefully. Examine the total annual percentage rate (APR), processing fees, and repayment dates so you know the exact cost of your financial stress relief.

- Receive Your Funds Directly in Your AccountAfter digital verification and e-mandate signing, the funds are disbursed directly into your registered bank account, often within a few hours, giving you the immediate liquidity you need.

- Execute Your Plan for Prompt RepaymentMark the repayment date clearly on your calendar or set up an auto-debit feature. Ensuring the necessary funds are available on payday maintains your relationship with the lender and boosts your credit profile.

Real-Life Examples of Month-End Relief

To truly appreciate how short-term loans help during month-end money problems, it helps to see how they function in everyday life. Here are five realistic scenarios where small, calculated borrowing makes all the difference:

The Utility Crunch: A salaried corporate professional faces an unexpectedly high summer electricity bill on the 26th; using a short-term loan lets them pay on time, avoiding disconnection and steep late penalties.

The Freelancer’s Gap: A freelance graphic designer experiences a ten-day client payment delay right when rent is due; they cover their landlord’s payment using a small instant loan and repay it the moment the invoice clears.

The Medical Emergency: A young family encounters an unplanned medical prescription expense on a weekend; they resolve the immediate cost through a short-term personal loan without touching their long-term equity investments.

The Commuter’s Fix: A bank employee’s scooter suffers a major engine breakdown halfway through the final week of the month; they fund the urgent vehicle repair using a quick salary advance loan to keep getting to work.

The Academic Deadline: A working professional pursuing a part-time certification needs to pay last-minute exam fees by the 28th; using a short-term online loan keeps them from missing the deadline and delaying their graduation.

Practical Tips for Using Short-Term Loans Responsibly

Short-term borrowing tips focus heavily on one main idea: credit is a tool. When used precisely, it is incredibly effective; when used carelessly, it can create unnecessary complications.

[ Borrow Only What You Need ]

│

▼

[ Compare Total Borrowing Costs ]

│

▼

[ Align Repayment with Payday ]

│

▼

[ Maintain a Cash Buffer Next Month ]

- Borrow Only What Is Absolutely Necessary: If you face a cash deficit of ₹5,000, borrow exactly ₹5,000. Do not be tempted to bump the amount up to ₹10,000 just because you qualify for it. Excess borrowing leads to unnecessary interest costs.

- Compare Interest Rates and Associated Fees: Look beyond the basic monthly interest rate. Check the processing fees, documentation charges, and pre-payment penalties to calculate the absolute cost of borrowing.

- Plan Your Repayment Strategy Before You Apply: Never sign a loan agreement without a concrete plan for how to pay it back. The ideal approach is to align the repayment auto-debit directly with your upcoming payday.

- Avoid Repeated and Continuous Reliance on Loans: Short-term loans are designed to be temporary fixes for unexpected gaps. If you find yourself needing to borrow every single month, it may be time to take a closer look at your core budget.

- Track Your Monthly Cash Flow Meticulously: Use a simple smartphone app or a basic Excel sheet to log your daily expenses. Gaining real-time visibility into where your money goes prevents late-month surprises.

Month-End Cash Management Checklist

| Checklist Point | Actionable Next Step |

| Expenses Tracked | Open your banking app and calculate exactly how much money you spent over the past three weeks. |

| Essential Bills Prioritized | Separate your non-negotiables (rent, electricity, food) from optional expenses (dining out, streaming services). |

| Loan Eligibility Checked | Visit EBORROW.IN to confirm you meet the age, income, and employment criteria. |

| Documents Ready | Save digital copies of your PAN, Aadhaar, and recent bank statements in a secure folder. |

| Short-Term Loan Amount Planned | Calculate the exact minimum shortfall amount required to reach your next payday safely. |

| Repayment Schedule Defined | Verify that your upcoming salary date aligns perfectly with the loan’s repayment timeline. |

| Alternative Funds Considered | Double-check if you have any small, secondary income streams or unused rewards points that could cover the gap. |

| Budget Adjusted for Next Month | Create a proactive plan to trim variable expenses next month to pay off the balance comfortably. |

| Impulse Purchases Minimized | Pause all online shopping carts and non-essential subscription payments until your cash flow balances out. |

| Financial Review Completed | Analyze why this month’s cash shortfall occurred to build stronger financial habits moving forward. |

Common Mistakes Beginners Make

When managing month-end financial help options for the first time, it is easy to make simple errors out of urgency. Being aware of these common behavioral pitfalls can save you time, money, and stress:

- Borrowing Significantly More Than Needed: It is easy to look at an approved credit limit and think, “Let me take a bit extra just in case.” This mistake increases your interest burden and leaves you with less take-home pay the following month.

- Ignoring the Specific Repayment Plan Details: Failing to read the exact date of your repayment auto-debit can lead to bounce charges from your bank. Always ensure your salary hits your account at least 24 to 48 hours before your loan payment is scheduled to withdraw.

- Using Multiple Loans Simultaneously: Taking out one small loan to pay off another creates a stressful debt loop. If you need financial support, use a single, structured loan from a transparent provider and focus entirely on paying it off.

- Skipping Crucial Lender Verification Steps: In a rush for quick funds, some borrowers turn to unverified, sketchy apps that operate outside regulatory guidelines. Always make sure your lender is a credible provider, like EBORROW.IN, that works with RBI-regulated partners.

- Overspending Immediately After Loan Disbursal: Receiving your loan funds can bring a wave of relief, but remember that money is earmarked for a specific emergency or bill. Spending it on non-essential items will leave you right back where you started.

Frequently Asked Questions (FAQs)

1. What is a short-term loan?

A short-term loan is a smaller, unsecured personal advance designed to cover temporary cash flow gaps. It features an expedited approval process and is meant to be paid back quickly, typically within a few weeks or months.

2. Who is eligible for a short-term loan?

Most salaried professionals and steady income earners in India aged 21 to 58 are eligible. You generally need to provide proof of consistent employment, valid KYC documents, and a functional savings account.

3. How fast are funds disbursed?

Thanks to modern, paperless digital verification systems, applications are processed quickly. Once approved and verified, funds can be deposited directly into your bank account within a few hours.

4. Can I repay my loan early?

Yes, most transparent digital lenders allow you to pay off your balance ahead of schedule. It is always wise to review your lender’s specific terms to see if they offer zero-foreclosure-fee options.

5. What interest rates should I expect?

Interest rates vary based on your individual credit profile, income levels, and the specific lender. Because these loans are unsecured and run for shorter periods, rates are calculated transparently relative to the shorter tenure.

6. Are there hidden fees I should look out for?

Reputable lenders list all charges clearly upfront. When reviewing your loan offer, look out for standard components like one-time processing fees, document verification costs, and late-payment penalties.

7. Can I apply for a short-term loan fully online?

Absolutely. The entire process—from uploading your document PDFs to signing your e-mandate—is done digitally from your smartphone or laptop, eliminating the need to visit a physical office.

8. How does a short-term loan affect my credit score?

Paying your loan back on time can actually help build a strong credit history over time. Conversely, missing your scheduled payments or delaying defaults will negatively affect your overall CIBIL rating.

9. How can I avoid over-borrowing?

Calculate your exact financial shortfall before applying and stick strictly to that amount. Treat the loan funds as dedicated capital for necessary expenses, rather than extra spending money.

10. When should I use a short-term loan instead of my savings?

Use a short-term loan when you face a temporary mismatch in timing—like a late salary or a sudden bill—and want to keep your long-term savings or investments working for you without interruption.

Conclusion

Experiencing a cash shortage at the end of the month is a common challenge, but it doesn’t have to disrupt your long-term financial health. When you understand how short-term loans help during month-end money problems, you can view these modern credit options as practical tools for managing temporary salary gaps. By keeping your essential expenses covered and your bills paid on time, a well-managed short-term loan can protect your credit score and give you valuable peace of mind.

The key to navigating these situations successfully is a commitment to responsible borrowing. By focusing on your actual needs, choosing transparent lending partners, and setting up a clear repayment plan, you can easily turn a stressful month-end cash crunch into a small, well-managed bump in the road.