Introduction

Month-end money pressure becomes stressful when urgent expenses arrive before salary. A medical bill, school fee, rent delay, travel emergency, home repair, or family responsibility can suddenly disturb a salaried person’s monthly budget. Even people with stable jobs can face short-term cash shortages because salary usually comes once a month, while expenses do not always wait.

This is where the topic Why Salaried Employees Need Quick Loan Options becomes important. A salaried employee usually has a fixed income, but fixed income does not always mean unlimited financial comfort. Many working professionals manage rent, groceries, EMIs, insurance, family support, education costs, transport, mobile bills, and lifestyle expenses from one monthly salary. If one unexpected expense appears, the whole budget can become unbalanced.

Beginners often feel confused when they search for quick loan options online. They see terms like personal loan, salary loan, short-term loan, instant approval, EMI, processing fee, credit score, tenure, prepayment, and interest rate. Without proper understanding, a person may apply quickly without checking the actual repayment cost. This can create financial pressure later.

Poor loan understanding can cause serious mistakes. Some people borrow more than they need. Some ignore hidden charges. Some choose a longer tenure without calculating total interest. Some miss repayment dates and damage their credit profile. Others depend on loans again and again instead of fixing their monthly budget. These mistakes do not happen because people are careless; they often happen because they are under pressure and do not have clear guidance.

This blog is created to explain quick loan options in a simple, practical, and responsible way. It will help salaried people understand what quick loans mean, when they are useful, when they should be avoided, how repayment works, what risks to check, and how to compare different borrowing options.

This guide is especially useful for salaried employees, first-time loan seekers, beginners in personal finance, young professionals, small business owners with fixed personal income, and people who want better money awareness. The purpose is not to encourage unnecessary borrowing. The purpose is to help readers make safer, smarter, and more informed financial decisions.

Quick decisions are common during money stress, but practical understanding is always better than panic borrowing. A quick loan option can be helpful during genuine urgency, but only when the borrower checks repayment capacity, total cost, terms, fees, and risk. A responsible borrower does not focus only on getting money fast; they also focus on paying it back comfortably.

Understanding Quick Loan Options in Simple Words

Quick loan options are borrowing choices that help people access money faster than traditional lengthy loan processes. For salaried employees, these options may include personal loans, salary-based loans, short-term loans, credit line facilities, overdraft options, or employer-linked salary advance support where available.

In simple words, a quick loan option means a loan that can be applied for with fewer steps, faster document checks, and quicker decision-making. However, “quick” should not be misunderstood as “free,” “risk-free,” or “always suitable.” Every loan comes with repayment responsibility.

Quick loans usually work by checking a borrower’s identity, income, employment status, bank details, credit profile, and repayment ability. A salaried employee may be seen as a relatively stable borrower because monthly income is predictable. However, approval, loan amount, interest rate, and tenure depend on the lender’s policy and the borrower’s profile.

People search for quick loan options because they need money during urgent situations. Common reasons include medical expenses, rent shortfall, school fees, emergency travel, family support, home repairs, unexpected bills, or temporary budget gaps before salary. In real life, quick loan options are used when waiting for long approval processes is difficult.

This topic connects directly with personal finance, borrowing, budgeting, credit score management, debt planning, and financial discipline. A loan is not only about receiving money; it is also about managing future cash flow. When you borrow today, you are using a portion of your future salary for repayment.

For example, suppose a salaried employee has a sudden medical expense before payday. Instead of using a high-cost informal borrowing source or delaying treatment, the employee may compare formal quick loan options, check EMI affordability, review charges, and borrow only the required amount. This is a more planned approach.

A common misunderstanding is that quick loans are always expensive or always dangerous. That is not fully correct. The risk depends on the lender, terms, interest rate, fees, repayment discipline, and borrower behavior. A quick loan can be useful if used carefully, but harmful if used casually.

The practical takeaway is simple: quick loan options are financial tools, not extra income. They should be used with planning, comparison, and repayment discipline.

Why Quick Loan Options Are Important for Salaried Employees

Quick loan options are important because salaried employees often have predictable income but limited short-term flexibility. Salary may be fixed, but life expenses are not always predictable. A sudden expense can appear at any time, and not everyone has a strong emergency fund ready.

From a savings point of view, quick loan options can prevent a person from breaking long-term savings for every small emergency. However, this is useful only when the loan cost is reasonable and repayment is manageable. If a person uses loans regularly for normal lifestyle spending, savings can reduce and debt pressure can increase.

From a borrowing perspective, quick loan options provide access to formal credit. Formal borrowing usually gives written terms, repayment schedules, interest details, and documentation. This is better than borrowing informally without clarity. Still, the borrower must read terms carefully.

For investing, quick loans should be treated with caution. Borrowing money to invest in stocks, crypto, trading, or risky assets can be dangerous for beginners. Market returns are not guaranteed, but loan repayment is mandatory. A salaried person should avoid using emergency loans for speculative activities.

For tax planning and financial records, loans also matter because borrowers should maintain clear records of repayment, interest, and bank transactions. In some cases, tax treatment depends on loan purpose and rules, so qualified advice may be needed.

Quick loan options also reduce emotional decision-making. When a person has a structured borrowing option, they are less likely to panic, sell important assets, or borrow from unsafe sources. However, emotional borrowing can still happen if someone applies without comparing options.

A practical scenario can explain this clearly. Imagine a salaried employee whose child’s school fee is due, but salary is delayed by a few days. A small short-term loan may help avoid penalty or stress. But if the employee borrows a larger amount for shopping at the same time, the loan becomes a burden. The difference is not the loan itself; the difference is the purpose and discipline.

The Real Problem Salaried Employees Face With Quick Loans

The real problem is not only lack of money. The bigger problem is lack of awareness during urgent financial pressure.

Many salaried people do not know how to calculate the real cost of borrowing. They may look only at the monthly EMI and ignore interest rate, tenure, processing fee, late payment charges, insurance charges, prepayment rules, and total repayment amount. This can make a loan look affordable when it is actually costly.

Another problem is confusing advice online. Some content makes loans look too easy. Some content makes all borrowing look dangerous. Beginners need balanced guidance. A loan can be helpful in genuine situations, but harmful when taken without purpose or repayment planning.

Emotional decision-making is also common. When people feel stressed, they want immediate relief. They may apply for the first loan offer they see. They may not compare lenders. They may not read the fine print. They may ignore whether the EMI fits their monthly budget.

Poor planning also creates repeated borrowing. If a person borrows every month to cover normal expenses, it shows a deeper budgeting issue. Quick loan options should not become a monthly habit for regular spending.

Weak comparison is another major issue. Many borrowers compare only the loan amount and approval speed. They forget to compare interest rate, total cost, customer support, repayment flexibility, and penalties.

Unrealistic expectations can also create problems. Some borrowers assume approval is guaranteed because they have a salary. But lenders may still check credit score, income stability, existing debt, documents, and repayment capacity.

Ignoring terms and conditions is a serious mistake. Loan documents contain important details about charges, repayment dates, default consequences, and borrower responsibilities. Not reading them can lead to unpleasant surprises later.

Depending only on social media advice is risky. A loan decision should be based on personal income, expenses, credit profile, and actual terms, not random opinions.

The right next step is to slow down before applying. Even if the loan process is quick, the decision should be thoughtful.

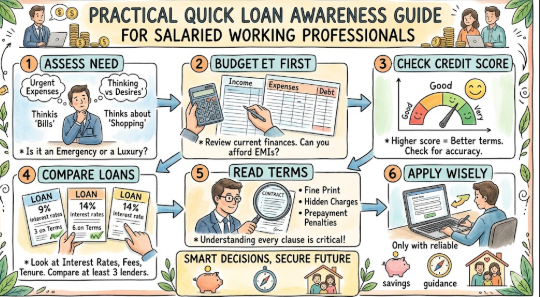

How Quick Loan Options Work Step by Step

Step 1: Identify the Actual Need

The first step is to understand why you need the loan. A genuine emergency is different from a lifestyle desire.

This matters because borrowing without a clear purpose can increase debt unnecessarily. Salaried employees should first check whether the expense is urgent, important, and unavoidable.

To apply this step, write down the exact expense. For example, “medical bill of ₹20,000” is clear. “Need extra money this month” is not clear enough.

A practical example: if your rent is due and salary is delayed, a short-term loan may be considered. But if you want a new phone without savings, borrowing may not be necessary.

The common mistake is borrowing more than required. The better approach is to borrow only the amount needed for the specific purpose.

Step 2: Check Your Monthly Budget

Before applying, review your income and expenses. A salaried person should know how much money remains after rent, groceries, bills, existing EMIs, insurance, and family responsibilities.

This matters because every loan creates a future repayment obligation. If your monthly budget is already tight, even a small EMI can create stress.

To apply this step, calculate your surplus income. If your salary is ₹50,000 and fixed expenses are ₹42,000, your available space is limited.

A practical example: if the new EMI is ₹5,000 but your monthly surplus is only ₹4,000, the loan may create pressure.

The common mistake is checking only loan eligibility. The better approach is checking repayment comfort.

Step 3: Review Your Credit Score and Existing Debt

Credit score and existing debt can influence loan eligibility and loan terms. A good credit profile may help in getting better terms, while missed payments can create difficulty.

This matters because lenders usually assess repayment behavior. Existing EMIs also reduce borrowing capacity.

To apply this step, check your current loans, credit card dues, and repayment history before applying.

A practical example: if you already have two EMIs and one credit card due, adding another loan may increase debt burden.

The common mistake is applying to many lenders at once without planning. The better approach is to compare first and apply carefully.

Step 4: Compare Loan Options

Do not select the first option only because it looks fast. Compare interest rate, EMI, tenure, processing fee, late charges, prepayment rules, and total repayment.

This matters because two loans with similar EMI may have different total costs.

To apply this step, create a simple comparison list before choosing.

A practical example: one lender may offer lower EMI but longer tenure, which may increase total interest. Another may have a higher EMI but lower total cost.

The common mistake is choosing the fastest option without checking the full cost. The better approach is balancing speed with affordability.

Step 5: Read Terms and Conditions Carefully

Loan terms explain your responsibilities. They include repayment date, charges, penalties, prepayment rules, default consequences, and documentation requirements.

This matters because hidden or ignored terms can create financial stress later.

To apply this step, read the loan agreement before accepting. If something is unclear, ask questions.

A practical example: some loans may charge a fee for early closure. If you plan to repay early, this matters.

The common mistake is clicking accept without reading. The better approach is to understand before signing.

Step 6: Calculate EMI and Total Repayment

EMI is important, but total repayment is equally important. A lower EMI may look comfortable, but a longer tenure can increase total cost.

This matters because salaried employees need monthly cash flow control.

To apply this step, use an EMI calculator or repayment sheet.

A practical example: if a loan EMI looks small but runs for many months, check total interest before deciding.

The common mistake is focusing only on EMI. The better approach is checking EMI plus total cost.

Step 7: Borrow Only What You Can Repay Comfortably

Responsible borrowing means taking a loan that fits your income, not the maximum amount available.

This matters because over-borrowing can damage savings, credit score, and mental peace.

To apply this step, keep EMI within a comfortable range based on your monthly obligations.

A practical example: even if you qualify for a higher loan amount, borrow only what solves the actual emergency.

The common mistake is treating loan eligibility as spending power. The better approach is treating eligibility as a limit, not a target.

Step 8: Repay on Time and Review Your Money Habits

After taking a loan, repayment discipline becomes the most important step. Missing EMIs can create penalties and affect credit profile.

This matters because one loan decision can influence future borrowing ability.

To apply this step, set payment reminders and keep enough balance before EMI date.

A practical example: if EMI is due on the 5th, keep the amount ready before the 4th.

The common mistake is forgetting repayment dates. The better approach is automating reminders and reviewing budget monthly.

Key Factors That Influence Quick Loan Options

Interest Rate

The interest rate is the cost of borrowing money. A higher interest rate increases repayment cost. Salaried employees should not judge a loan only by approval speed. They should compare interest rates carefully and understand whether the rate is fixed or variable.

EMI

EMI is the monthly amount paid toward the loan. It includes principal and interest. A manageable EMI helps protect monthly cash flow. The mistake many beginners make is accepting an EMI that looks possible on paper but becomes difficult after normal expenses.

Repayment Capacity

Repayment capacity means your ability to pay the loan without disturbing essential expenses. It depends on salary, existing EMIs, rent, family expenses, savings, and financial responsibilities. A better approach is to calculate repayment capacity before applying.

Credit Score

Credit score reflects borrowing and repayment behavior. Timely repayments can support a healthier credit profile, while missed payments can create problems. Salaried employees should check credit health regularly instead of thinking about it only during loan applications.

Hidden Charges

Some loans may include processing fees, late payment charges, documentation fees, foreclosure charges, or other costs. These charges can increase total borrowing cost. The better approach is to ask for a full cost breakdown.

Loan Tenure

Loan tenure is the repayment period. A longer tenure may reduce EMI but increase total interest. A shorter tenure may reduce total interest but increase monthly EMI. Borrowers should choose tenure based on comfort and total cost.

Processing Fees

Processing fee is charged by some lenders for handling the loan application. It may be deducted from the disbursed amount or charged separately. Beginners should check this before accepting the loan.

Prepayment Rules

Prepayment means paying the loan before the scheduled end date. Some lenders allow it easily, while others may charge fees. If you expect bonus, incentive, or salary arrears, prepayment flexibility may be useful.

Detailed Breakdown of Quick Loan Options for Salaried Employees

What a Quick Loan Means

A quick loan is a borrowing option designed to provide faster access to funds. It may involve online application, digital document submission, faster verification, and quicker decision-making. But quick access does not remove the responsibility of repayment.

For salaried employees, quick loans are often linked to income proof, salary slips, bank statements, employment details, and credit history. The lender checks whether the borrower has a stable repayment source.

When Borrowing Makes Sense

Borrowing may make sense when the expense is necessary, urgent, and cannot be managed through savings or delayed payment. Examples include medical needs, emergency travel, essential repairs, education fees, or temporary salary delay.

A loan may also be considered when it prevents a bigger financial problem. For example, paying an urgent bill on time may avoid penalty or service disruption. But this should still be done with repayment planning.

When Borrowing Should Be Avoided

Borrowing should be avoided for unnecessary lifestyle upgrades, impulsive shopping, risky investing, speculative trading, gambling, or repeated monthly shortfalls. If a person borrows for non-essential spending, the loan may create long-term stress.

A loan should also be avoided when repayment is uncertain. If job stability is weak or existing debt is already high, borrowing more can increase risk.

Eligibility Basics

Eligibility usually depends on income, employment type, salary consistency, credit profile, existing debt, age, documents, and lender policy. Salaried employees may have an advantage because income is regular, but this does not mean approval is guaranteed.

Beginners should understand that eligibility is not the same as affordability. A lender may approve an amount, but the borrower must decide whether repayment is comfortable.

Interest Rate Understanding

Interest rate directly affects loan cost. Even a small difference in rate can matter over time. Borrowers should ask whether the rate is monthly or annual, fixed or floating, and whether any additional charges apply.

The better approach is to compare the annual cost and total repayment, not just the advertised EMI.

EMI and Repayment Planning

EMI should fit comfortably into the monthly salary structure. Salaried employees should plan EMI after accounting for rent, groceries, bills, transport, insurance, school fees, family support, and savings.

A good repayment plan includes reminders, bank balance planning, and emergency buffer. Missing EMI should be avoided because it can lead to charges and credit impact.

Hidden Charges and Processing Fees

A loan may look affordable until charges are added. Processing fees, late fees, prepayment charges, documentation fees, and penalty charges must be reviewed carefully.

The better approach is to ask, “What is the total amount I will pay from start to finish?”

Credit Score Impact

Loan behavior can affect credit profile. Timely repayment may support credit discipline. Missed EMI, defaults, or excessive loan applications may create problems.

Salaried people should treat every loan as part of their long-term financial reputation.

Debt Burden

Debt burden increases when multiple EMIs consume too much salary. Even if each EMI looks small, combined EMIs can reduce savings and create stress.

The better approach is to keep debt controlled and avoid taking a new loan to repay old unnecessary debt unless proper restructuring advice is taken.

Responsible Borrowing

Responsible borrowing means borrowing for the right reason, choosing affordable terms, reading documents, protecting personal data, and repaying on time. It also means saying no to a loan when it is not needed.

Loan Comparison Basics

When comparing loans, check:

- Interest rate

- EMI

- Total repayment

- Tenure

- Processing fee

- Late payment charges

- Prepayment rules

- Customer support

- Documentation clarity

- Data privacy practices

Prepayment and Late Payment Impact

Prepayment may help reduce debt faster, but rules should be checked. Late payment can lead to penalties and credit issues. Borrowers should understand both before accepting the loan.

Common Mistakes Beginners Make With Quick Loan Options

Following Random Advice

This happens when people trust friends, social media, or online comments without checking their own financial situation. It is risky because every borrower has different income, expenses, and repayment capacity. The better approach is to compare options based on your own budget.

Ignoring Risk

Some borrowers focus only on receiving money quickly. They forget that repayment is compulsory. This can create EMI stress later. The better approach is to check risk before accepting funds.

Not Comparing Options

Choosing the first loan offer may lead to higher costs. Borrowers should compare interest rates, fees, tenure, and total repayment. The better approach is to review at least a few suitable options before applying.

Trusting Fake Claims

Any claim that sounds too easy, too fast, or guaranteed should be checked carefully. Financial decisions should not be based on unrealistic promises. The better approach is to verify lender details and read terms.

Ignoring Hidden Charges

Processing fees, penalties, and prepayment charges can increase cost. Borrowers should ask for complete cost details. The better approach is to calculate total repayment.

Making Emotional Decisions

Stress can push people into fast decisions. Panic borrowing may create long-term debt. The better approach is to pause, calculate, compare, and then decide.

Using Emergency Money for Risky Activities

Borrowed money should not be used for speculative trading, crypto bets, gambling, or risky investments. The better approach is to keep loans for genuine needs.

Not Reading Terms and Conditions

Loan terms explain charges and responsibilities. Ignoring them can cause surprises. The better approach is to read before accepting.

Sharing Sensitive Information Carelessly

Borrowers should protect Aadhaar, PAN, bank details, OTPs, passwords, and salary documents. The better approach is to share information only through trusted and secure channels.

Depending Only on Social Media Advice

Social media can give ideas, but it cannot replace personal financial review. The better approach is to use social media only as general awareness, not final advice.

Don’t Do This Checklist

- Do not borrow without knowing the exact need.

- Do not accept a loan only because approval looks fast.

- Do not ignore interest rate and fees.

- Do not miss EMI dates.

- Do not borrow for unnecessary shopping.

- Do not use loans for risky trading or gambling.

- Do not share OTPs or passwords.

- Do not apply to many lenders randomly.

- Do not ignore your credit score.

- Do not sign without reading terms.

Practical Real-Life Examples of Quick Loan Options

Example 1: Salaried Person Managing Month-End Expenses

Rohit receives his salary on the last day of every month, but an urgent medical bill arrives five days earlier. His mistake would be borrowing a large amount without checking EMI. A better action is to calculate the exact need, compare loan charges, and borrow only the required amount. The learning is that quick loans should solve a specific problem, not create extra spending.

Example 2: Employee Avoiding Credit Card Debt Pressure

Priya uses her credit card for an emergency repair but realizes the repayment may become expensive if delayed. Instead of rolling over the card balance, she compares a structured loan option with fixed EMI. The better action is choosing the option with clearer repayment terms. The learning is that structured repayment can sometimes be better than unclear debt continuation.

Example 3: Loan Seeker Comparing Repayment Options

Amit needs funds for education fees. He sees two loan offers: one with lower EMI and longer tenure, another with higher EMI and shorter tenure. His challenge is understanding total cost. The better action is to compare total repayment, not only monthly EMI. The learning is that lower EMI does not always mean cheaper borrowing.

Example 4: Small Business Owner With Salary-Like Income

Neha runs a small business but pays herself a fixed monthly amount. She needs money for a family emergency. Her mistake would be mixing business funds and personal loans without records. A better action is to maintain clear repayment planning and documentation. The learning is that financial clarity matters even when income is regular.

Example 5: Young Professional Avoiding Lifestyle Borrowing

Karan wants to buy an expensive gadget before receiving his bonus. He considers a quick loan but realizes it is not urgent. The better action is waiting, saving, or buying later. The learning is that not every desire needs a loan, even if loan options are available.

Two Useful Tables for Better Understanding

Table 1: Quick Loan Decision Comparison

| Situation | Borrowing May Help | Borrowing May Be Risky | Better Approach |

|---|---|---|---|

| Medical emergency | When funds are needed urgently | If repayment capacity is ignored | Borrow only required amount |

| Salary delay | When essential bills are due | If used for extra shopping | Match loan amount with shortfall |

| Education fee | When deadline is near | If tenure and charges are unclear | Compare total repayment |

| Lifestyle purchase | Usually avoidable | Can create unnecessary debt | Save and buy later |

| Existing EMI pressure | Only with proper advice | Can increase debt burden | Review budget first |

Table 2: Beginner Mistake vs Correct Approach

| Beginner Mistake | Why It Is Risky | Correct Approach |

|---|---|---|

| Checking only EMI | Total cost may be higher | Check EMI and total repayment |

| Borrowing maximum eligible amount | Can increase debt pressure | Borrow only what is needed |

| Ignoring fees | Final cost may rise | Review all charges |

| Missing repayment dates | Can affect credit profile | Set reminders and auto-pay |

| Applying without comparison | May lead to costly terms | Compare multiple suitable options |

| Sharing data carelessly | Fraud risk increases | Use secure and trusted channels |

Tools, Methods, and Frameworks Readers Can Use

EMI Calculator

An EMI calculator helps estimate monthly repayment. It is useful because salaried employees can check whether the EMI fits their salary. Beginners should use it before applying, not after accepting the loan. It helps avoid the mistake of choosing unaffordable repayment.

Repayment Planning Sheet

A repayment planning sheet records loan amount, EMI date, tenure, charges, and balance. It helps borrowers stay organized. Beginners can create a simple spreadsheet and update it monthly. This avoids missed payments and confusion.

Credit Score Review

A credit score review helps borrowers understand their credit health. It matters because repayment behavior can affect future borrowing options. Beginners should check credit reports for errors and avoid late payments.

Loan Comparison Checklist

A loan comparison checklist helps compare interest rate, processing fee, tenure, total repayment, late fees, and prepayment rules. It prevents rushed decisions. Beginners can use this before selecting any lender.

Debt-to-Income Review Method

This method compares monthly debt payments with monthly income. It helps salaried employees understand whether they already have too much debt. It avoids over-borrowing and protects monthly cash flow.

Emergency Fund Method

An emergency fund is money kept aside for urgent expenses. It reduces dependence on loans. Beginners can start small by saving a fixed amount every month. This helps avoid repeated borrowing.

Monthly Money Review System

A monthly review helps track income, expenses, debt, and savings. Salaried employees can do this after salary day. It helps identify spending leaks and reduces the need for quick loans.

Expert Tips to Make Better Loan Decisions

1. Borrow for Need, Not Desire

This matters because loans create repayment responsibility. Use loans for genuine needs such as emergencies or essential payments. Avoid borrowing for impulse purchases.

2. Compare Before Applying

Comparison helps reduce costly mistakes. Check interest rate, EMI, tenure, fees, and total repayment. Do not select an option only because it looks fast.

3. Check Repayment Comfort

A loan is safe only when repayment fits your budget. Calculate monthly expenses before accepting EMI. Leave room for savings and emergencies.

4. Read Terms Carefully

Terms explain your legal and financial responsibility. Read charges, penalties, and repayment rules. Ask questions if something is unclear.

5. Avoid Multiple Random Applications

Too many applications can create confusion and may affect your credit profile. Shortlist suitable options first. Apply only after proper comparison.

6. Keep Emergency Money Separate

Emergency funds reduce loan dependency. Even small savings can help during urgent needs. Do not use emergency money for unnecessary spending.

7. Protect Personal Data

Loan applications require sensitive information. Share documents only with trusted platforms. Never share OTPs, passwords, or banking PINs.

8. Avoid Borrowing for Risky Activities

Do not use loans for trading, crypto speculation, gambling, or fake profit schemes. Loan repayment is fixed, but returns are uncertain.

9. Track EMI Dates

Missing EMI can create penalties and credit issues. Set reminders before due dates. Keep bank balance ready in advance.

10. Understand Total Cost

A low EMI may hide a longer tenure. Always check total repayment amount. Choose a structure that balances monthly comfort and total cost.

11. Keep Written Records

Maintain loan documents, payment receipts, and communication records. This helps avoid disputes and confusion. Organized records support better financial control.

12. Review Budget After Taking a Loan

A new EMI changes your monthly budget. Reduce unnecessary expenses until the loan is repaid. This prevents debt pressure.

13. Take Professional Advice When Needed

If the loan is large or terms are confusing, consult a qualified financial professional. Advice can help avoid costly mistakes.

14. Avoid Pressure-Based Decisions

Do not borrow because someone is pushing you. Take time to understand the terms. A calm decision is usually better than a rushed one.

15. Learn From Every Loan Experience

After repayment, review what went right and wrong. This improves future money decisions. Good borrowers become better planners over time.

Case Studies: How Better Understanding Changes Decisions

Case Study 1: The Salary Delay Situation

Profile: Ankit, a salaried employee living in a rented apartment.

Situation: His salary was delayed by one week, but rent and electricity bills were due.

Problem: He had no emergency fund and felt pressured to borrow quickly.

Wrong Approach: He considered borrowing more than required because the approved amount was higher.

Better Approach: He calculated the exact shortfall, compared repayment terms, and borrowed only the amount needed for rent and bills.

Result or Learning: His EMI stayed manageable, and he started building a small emergency fund after salary was received.

Key Takeaway: Borrowing only what is necessary reduces repayment pressure.

Case Study 2: The Credit Card Trap

Profile: Meena, a young professional with regular salary and credit card usage.

Situation: She used her credit card for an emergency home repair.

Problem: She could not pay the full credit card bill immediately.

Wrong Approach: She thought of paying only the minimum due for several months.

Better Approach: She compared structured repayment options and chose a plan with clear EMI and defined repayment schedule.

Result or Learning: She understood the importance of comparing debt costs and stopped using credit cards for unplanned spending.

Key Takeaway: Clear repayment planning is better than continuing unclear debt.

Case Study 3: The Lifestyle Loan Mistake

Profile: Saurabh, a salaried employee who recently received a salary hike.

Situation: He wanted to buy expensive electronics and planned to take a quick loan.

Problem: The purchase was not urgent, and he already had an existing EMI.

Wrong Approach: He almost accepted the loan because approval looked easy.

Better Approach: He reviewed his budget and decided to save for three months instead.

Result or Learning: He avoided unnecessary debt and improved his saving habit.

Key Takeaway: Quick loan options should not replace financial discipline.

Risk Awareness: What Readers Must Check First

Interest Rate Risk

Interest rate risk means the loan may cost more than expected if the borrower does not understand the rate clearly. It matters because higher cost increases EMI pressure. Reduce this risk by comparing rates and total repayment.

Credit Risk

Credit risk means missed payments can affect your credit profile. It matters because future loan options may become difficult. Reduce this risk by paying EMIs on time.

Over-Borrowing Risk

Over-borrowing happens when a person takes more money than needed. It matters because higher debt creates long-term pressure. Reduce this risk by borrowing only for the actual need.

Fraud Risk

Fraud risk includes fake lenders, unsafe links, document misuse, or OTP scams. It matters because personal and financial data can be misused. Reduce this risk by using trusted channels and protecting sensitive information.

Data Privacy Risk

Loan applications require personal documents. If shared carelessly, privacy can be affected. Reduce this risk by checking platform credibility and avoiding unknown links.

Emotional Risk

Stress, fear, or urgency can lead to poor borrowing decisions. It matters because panic borrowing may create bigger problems. Reduce this risk by pausing, calculating, and comparing.

Legal or Compliance Risk

Loan agreements are legal documents. Ignoring terms can lead to disputes or penalties. Reduce this risk by reading all documents before acceptance.

Misinformation Risk

Online advice may be incomplete or misleading. It matters because wrong guidance can lead to bad decisions. Reduce this risk by verifying details and consulting qualified professionals where needed.

Debt Cycle Risk

Debt cycle risk happens when one loan leads to another. It matters because salary gets consumed by repayments. Reduce this risk by budgeting and avoiding repeated borrowing.

Checklist Before Taking Action

Before applying for any quick loan option, check the following:

- I understand why I need the loan.

- I have calculated the exact amount required.

- I have checked my monthly income and expenses.

- I know how much EMI I can afford.

- I have compared multiple suitable loan options.

- I have checked interest rate and total repayment.

- I have reviewed processing fees and hidden charges.

- I have read repayment terms and late payment rules.

- I have checked prepayment or foreclosure conditions.

- I have avoided fake approval or guaranteed claims.

- I have kept emergency funds separate where possible.

- I have protected my personal and financial data.

- I have avoided borrowing for risky investments or gambling.

- I have reviewed tax, legal, or compliance impact if relevant.

- I have prepared a written repayment plan.

- I have avoided panic-based decisions.

- I have considered professional advice if the loan is large or confusing.

Use this checklist before making any borrowing decision. A quick loan process should not mean a careless loan decision. Even a few minutes of review can protect you from unnecessary charges, repayment stress, and future credit problems.

Strategic Insights for Better Decision-Making

Debt-to-Income Ratio

Debt-to-income ratio shows how much of your income goes toward debt repayment. If too much salary is already going into EMIs, a new loan can create stress. Beginners can calculate this by adding all EMIs and comparing them with monthly salary.

EMI Burden

EMI burden means the pressure created by monthly repayments. A salaried employee should ensure that EMI does not disturb rent, food, transport, insurance, and savings. The better approach is to keep EMI realistic.

Credit Score Management

Credit score management means paying on time, avoiding unnecessary applications, and keeping debt under control. A good credit habit supports future financial flexibility.

Prepayment Planning

If you expect bonus, incentive, or extra income, you may plan early repayment. But check whether prepayment charges apply. This can reduce debt faster when done correctly.

Loan Restructuring Awareness

If repayment becomes difficult, some borrowers may need restructuring or professional guidance. Ignoring the problem can make it worse. The better approach is to speak to the lender early and understand available options.

Short-Term vs Long-Term Debt Impact

Short-term loans may close faster but have higher monthly pressure. Long-term loans may reduce EMI but increase total cost. Salaried employees should balance monthly comfort with total repayment.

Emergency Fund Planning

A strong emergency fund reduces the need for quick borrowing. Beginners can start with a small monthly saving target. Over time, this creates financial confidence.

Lifestyle Inflation Control

When salary increases, expenses often increase too. This is called lifestyle inflation. If every salary hike leads to new EMIs, financial growth becomes weak. The better approach is to increase savings along with income.

Key Terms Explained for Beginners

- Quick Loan: A loan option designed for faster application, verification, and disbursal. It should still be reviewed carefully before acceptance.

- Salaried Employee: A person who receives fixed income from employment, usually every month. Regular income can help with repayment planning.

- Interest Rate: The cost of borrowing money. A higher interest rate increases total repayment.

- EMI: Equated Monthly Instalment. It is the fixed monthly payment made toward loan repayment.

- Loan Tenure: The time period over which the loan is repaid. Longer tenure may reduce EMI but increase total interest.

- Processing Fee: A charge taken by some lenders for processing the loan application.

- Credit Score: A number that reflects repayment behavior and credit history. Timely payments help maintain better credit health.

- Repayment Capacity: The borrower’s ability to repay the loan comfortably without disturbing essential expenses.

- Prepayment: Paying part or full loan amount before the scheduled end date. Rules and charges should be checked.

- Late Payment Charge: A penalty charged when EMI is not paid on time.

- Debt Burden: The pressure created when too much income goes toward loan repayments.

- Hidden Charges: Extra costs that may not be obvious at first, such as penalties, fees, or service charges.

- Emergency Fund: Savings kept aside for urgent expenses. It helps reduce dependence on loans.

- Loan Agreement: A legal document that explains loan terms, charges, repayment schedule, and borrower responsibilities.

- Responsible Borrowing: Borrowing only when needed, comparing options, understanding terms, and repaying on time.

Who Should Read This Blog

Beginners

Beginners who do not understand loans, EMI, interest rates, and repayment terms will find this guide useful. It explains borrowing in simple language.

Students

Students preparing for jobs or managing education-related expenses can learn how borrowing works and why repayment discipline matters.

Salaried Employees

Salaried people are the main audience for this blog. It helps them understand quick loan options, salary-based repayment planning, and debt control.

Small Business Owners

Small business owners with fixed personal income can learn how to separate personal borrowing from business cash flow.

New Investors

New investors should understand why borrowing for risky investments can be dangerous. This blog explains why loans should not be treated as investment capital.

Traders

Traders can learn why taking loans for trading is risky. Market returns are uncertain, but loan repayment is fixed.

Loan Seekers

Loan seekers can use this blog to compare options, check costs, and avoid common mistakes before applying.

Crypto Learners

Crypto learners can understand why borrowed money should not be used for speculative crypto decisions.

Casino Content Creators

Casino content creators can learn responsible financial language and risk-aware content thinking when discussing money-related topics.

Finance Bloggers

Finance bloggers can use this structure to create helpful, responsible, and beginner-friendly loan awareness content.

People Improving Money Awareness

Anyone trying to avoid financial mistakes can benefit from the checklists, examples, and case studies in this guide.

Frequently Asked Questions

1. What does Why Salaried Employees Need Quick Loan Options mean?

Why Salaried Employees Need Quick Loan Options means understanding why people with fixed monthly income may need faster borrowing support during urgent expenses. It also means learning how to borrow responsibly, compare terms, and repay safely.

2. Are quick loan options useful for salaried people?

Yes, quick loan options can be useful during genuine emergencies such as medical bills, rent gaps, education fees, or urgent repairs. However, they should be used only after checking repayment capacity, charges, and terms.

3. What is the biggest mistake salaried employees make with quick loans?

The biggest mistake is focusing only on fast approval and ignoring total repayment cost. Borrowers should compare interest rate, EMI, tenure, processing fee, late charges, and prepayment rules before accepting a loan.

4. Is loan approval guaranteed for salaried employees?

No, loan approval is not guaranteed. Lenders may check income, employment stability, credit score, existing debt, documents, and internal policies before making a decision.

5. How can I know whether an EMI is affordable?

Calculate your monthly income after essential expenses like rent, food, bills, insurance, transport, and existing EMIs. If the new EMI leaves no savings or emergency space, it may not be comfortable.

6. Why Salaried Employees Need Quick Loan Options during emergencies?

Salaried employees may face urgent expenses before payday or during salary delays. Quick loan options can help manage short-term gaps, but they should be used with clear repayment planning and cost comparison.

7. Should I use a quick loan for investing or trading?

Beginners should avoid using borrowed money for investing, trading, crypto, or gambling. Returns are uncertain, but loan repayment is fixed. This can create serious financial pressure.

8. What charges should I check before taking a quick loan?

Check interest rate, processing fee, late payment charges, prepayment fee, documentation fee, and total repayment amount. Do not accept a loan without understanding all costs.

9. Can a quick loan affect my credit score?

Yes, repayment behavior can affect your credit profile. Timely EMI payments support credit discipline, while missed payments can create negative impact.

10. Why Salaried Employees Need Quick Loan Options instead of informal borrowing?

Formal quick loan options may provide written terms, structured repayment, and clearer documentation. Informal borrowing may lack transparency. Still, formal loans must be compared and reviewed carefully.

11. How often should I review my loan and budget?

Review your budget every month, especially after salary day. Track EMI, expenses, savings, and upcoming payments. Monthly review helps prevent repeated borrowing.

12. What is the best next step before applying for a loan?

The best next step is to calculate the exact need, check repayment capacity, compare loan options, read terms, and prepare a written repayment plan. Do not apply in panic.

Conclusion and Next Steps

Understanding Why Salaried Employees Need Quick Loan Options is important because financial emergencies can happen even when income is stable. A monthly salary provides structure, but it does not always protect a person from sudden expenses. Medical needs, rent pressure, education fees, family emergencies, repairs, or salary delays can create short-term cash gaps.

Quick loan options can be helpful in such situations, but only when used responsibly. The main lesson is that a loan is not extra income. It is borrowed money that must be repaid from future salary. This is why every salaried employee should check purpose, repayment capacity, interest rate, EMI, tenure, charges, and terms before applying.

Beginners should avoid panic borrowing. A fast loan process does not mean the decision should be fast and careless. Even during urgency, it is possible to pause for a few minutes, calculate the exact need, compare options, and read important terms. This small effort can prevent long-term financial stress.

The blog also explained that borrowing should not be used for risky activities such as speculative trading, crypto bets, gambling, or unnecessary lifestyle purchases. Salaried employees should protect their monthly cash flow because salary supports essential expenses, family responsibilities, savings, and financial goals.

A better approach is to build strong money habits. Create an emergency fund, review your budget monthly, track EMIs, protect personal data, avoid fake claims, and use loans only when they truly solve a practical problem. If the loan amount is large or terms are confusing, professional advice should be considered.

The next step is simple. Before taking any quick loan, use the checklist in this blog. Write down your need, calculate repayment comfort, compare costs, check terms, and decide calmly. If the loan helps you manage a genuine emergency without disturbing your long-term financial health, it may be useful. If it adds unnecessary pressure, it may be better to wait, save, or explore safer alternatives.

Financial awareness is not about avoiding every loan. It is about knowing when to borrow, how much to borrow, from where to borrow, and how to repay without damaging your future. Salaried employees who understand this can handle urgent needs with more confidence, discipline, and control.