Introduction

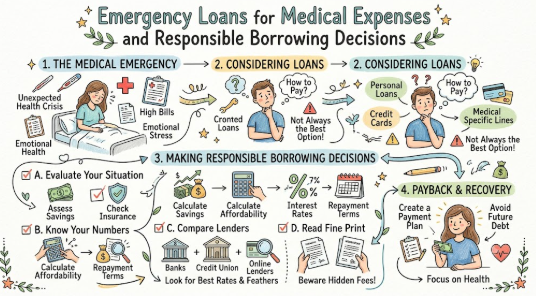

A medical emergency often arrives without warning, and the stress becomes heavier when hospital bills, medicines, tests, surgery costs, or recovery expenses come before salary or savings. Many beginners feel confused because they do not know whether to use savings, borrow from family, use a credit card, take a personal loan, or apply for an emergency loan. In panic, people may accept the first loan offer without checking interest rate, EMI, charges, repayment terms, or their monthly capacity. This can create long-term debt pressure. Understanding How to Manage Sudden Medical Expenses With Emergency Loans helps readers make practical, calm, and safer financial decisions during a difficult time. This guide is for salaried employees, families, loan seekers, and anyone who wants to handle urgent medical expenses without making careless borrowing mistakes.

Understanding Emergency Loans for Medical Expenses in Simple Words

An emergency loan is a loan taken to manage urgent expenses when immediate funds are required. In the case of medical needs, it may be used for hospital admission, surgery, medicines, diagnostic tests, post-treatment care, travel for treatment, or temporary income gaps during recovery.

In simple words, an emergency medical loan helps you arrange money quickly, but it is still a financial responsibility. It is not free money. You must repay it with interest, charges, and agreed EMIs.

People search for this topic when they face sudden expenses and do not have enough savings or insurance coverage. It connects directly with personal finance because it affects monthly cash flow, borrowing capacity, credit score, and future financial planning.

Beginner-friendly example:

Suppose a salaried person needs ₹80,000 for a family member’s emergency treatment. Their savings cover only ₹30,000. They may consider an emergency loan for the remaining ₹50,000 after checking EMI, interest rate, processing fee, and repayment tenure.

Common misunderstanding:

Many beginners think emergency loans are automatically safe because they are used for medical needs. But the purpose may be genuine while the borrowing terms may still be expensive.

Practical takeaway:

Use emergency loans only after checking total repayment cost, EMI comfort, and other available options.

Why Emergency Medical Loan Planning Is Important

Medical expenses affect real-life financial decisions because they can disturb savings, monthly budgets, debt plans, and family stability. A sudden bill can force people to withdraw emergency funds, delay other payments, or take high-cost debt.

Emergency medical loan planning is important because it helps you decide how much to borrow, how long to repay, and how to avoid unnecessary debt pressure.

It also improves risk awareness. Instead of taking a loan emotionally, you compare options, check terms, protect personal data, and avoid misleading offers. A planned approach can also protect your credit score because missed EMIs may affect future borrowing.

Short practical scenario:

A person with ₹40,000 monthly income takes a large loan without checking EMI. Later, the EMI consumes too much income, causing delayed rent and credit card payments. A better approach would be to borrow only the required amount and choose an EMI that fits the monthly budget.

The Real Problem Readers Face With Medical Expenses

The biggest problem is not only the hospital bill. The real problem is confusion under pressure.

During a medical emergency, families may face:

- Lack of awareness about loan options

- Too much confusing advice online

- Emotional decision-making

- Weak comparison of interest rates and charges

- Unrealistic expectations about approval

- Not reading terms and conditions

- Ignoring repayment capacity

- Depending only on social media advice

- Sharing personal details with unknown loan agents

- Not knowing the right next step

A beginner may think, “I need money now, so any loan is fine.” But this mindset can create future stress. Medical emergencies are emotional, but loan decisions should still be practical.

Better approach:

Take a few minutes to check the amount needed, available savings, insurance support, loan cost, EMI, repayment period, and lender credibility before applying.

How to Manage Sudden Medical Expenses With Emergency Loans Step by Step

Step 1: Calculate the Exact Medical Requirement

What it means:

Find out how much money is actually needed for treatment, tests, medicines, room charges, and follow-up care.

Why it matters:

Borrowing more than required increases EMI burden. Borrowing less than required may create another shortage.

How to apply it:

Ask the hospital for an estimated bill and include extra funds for medicines, tests, and recovery.

Practical example:

If the hospital estimate is ₹70,000, do not blindly borrow ₹1,50,000. First check what is urgent and what can be covered from savings or insurance.

Common mistake:

Taking a large loan in panic.

Better approach:

Borrow the minimum practical amount needed after calculating available funds.

Step 2: Check Your Savings and Insurance First

What it means:

Before applying for a loan, check emergency savings, health insurance, employer medical benefits, and family support.

Why it matters:

A loan should fill the gap, not replace every available option.

How to apply it:

Review your insurance policy, claim process, cashless hospital support, and reimbursement option.

Practical example:

If insurance covers ₹60,000 from a ₹1,00,000 bill, you may need a loan only for ₹40,000 plus small extra costs.

Common mistake:

Taking a loan without checking insurance coverage.

Better approach:

Use insurance and savings first, then borrow only the remaining amount.

Step 3: Compare Loan Options Carefully

What it means:

Compare different borrowing options such as personal loans, salary advance, employer loan, credit line, or family support.

Why it matters:

Different options have different interest rates, fees, repayment terms, and risks.

How to apply it:

Compare interest rate, EMI, processing fee, prepayment charges, late payment penalties, and lender credibility.

Practical example:

A lower EMI may look attractive, but a longer tenure can increase total interest cost.

Common mistake:

Choosing the first loan offer.

Better approach:

Compare at least a few suitable options before deciding.

Step 4: Check EMI Affordability

What it means:

EMI affordability means checking whether you can repay the loan comfortably from monthly income.

Why it matters:

Medical stress should not become long-term debt stress.

How to apply it:

List monthly income, rent, food, school fees, existing EMIs, insurance, and basic expenses before choosing EMI.

Practical example:

If your monthly income is ₹45,000 and existing expenses are ₹38,000, a high EMI may not be safe.

Common mistake:

Looking only at approval amount, not repayment comfort.

Better approach:

Choose an EMI that allows you to manage regular expenses without missing payments.

Step 5: Read Terms and Conditions

What it means:

Loan terms explain interest, fees, penalties, tenure, repayment schedule, and borrower responsibilities.

Why it matters:

Hidden charges can increase total cost.

How to apply it:

Read processing fee, foreclosure charges, late fee, bounce charges, insurance add-ons, and prepayment rules.

Practical example:

A loan may advertise a low rate but include high processing or penalty charges.

Common mistake:

Signing without reading the full loan agreement.

Better approach:

Ask questions before accepting the loan.

Step 6: Protect Your Personal and Financial Data

What it means:

Emergency borrowers may share Aadhaar, PAN, bank details, salary slips, and medical documents.

Why it matters:

Sharing sensitive data with unknown sources can create fraud risk.

How to apply it:

Use trusted lenders, official platforms, secure documents, and avoid sending OTPs to anyone.

Practical example:

A fake loan agent may ask for upfront fees or OTP verification. This can be risky.

Common mistake:

Sharing documents through random messages.

Better approach:

Apply only through verified channels and never share OTPs or passwords.

Step 7: Plan Repayment Before Taking the Loan

What it means:

Decide how you will repay the loan before accepting it.

Why it matters:

A repayment plan prevents missed EMIs and credit score damage.

How to apply it:

Set EMI reminders, adjust monthly spending, pause non-essential expenses, and keep a small buffer.

Practical example:

If EMI starts next month, reduce entertainment, subscriptions, or non-urgent purchases for a few months.

Common mistake:

Thinking about repayment after taking the loan.

Better approach:

Create a repayment plan before borrowing.

Step 8: Review the Loan After the Emergency

What it means:

Once the medical situation stabilizes, review your loan, expenses, and repayment strategy.

Why it matters:

You may find ways to prepay, reduce cost, or rebuild savings.

How to apply it:

Check outstanding balance, prepayment rules, monthly cash flow, and emergency fund rebuilding plan.

Practical example:

If you receive a bonus, you may partly repay the loan if there are no heavy prepayment charges.

Common mistake:

Ignoring the loan after treatment is complete.

Better approach:

Review repayment every month until the loan is closed.

Key Factors That Influence Emergency Medical Loans

Interest Rate

The interest rate is the cost of borrowing. A higher rate increases total repayment. Beginners should compare rates carefully, but they should also check fees and terms because a low rate alone does not always mean the cheapest loan.

EMI

EMI is the monthly payment you make to repay the loan. It should fit your income and expenses. A comfortable EMI is better than an aggressive EMI that causes missed payments.

Repayment Capacity

Repayment capacity means your ability to pay EMIs without disturbing essential expenses. It depends on income, existing loans, family responsibilities, and monthly budget.

Credit Score

Your credit score may influence eligibility, loan amount, interest rate, and approval process. Paying EMIs on time can support credit health, while missed payments may damage it.

Hidden Charges

Processing fees, late fees, bounce charges, insurance add-ons, and prepayment penalties can increase total loan cost. Always check the full cost before accepting.

Loan Tenure

Tenure is the repayment period. Longer tenure may reduce EMI but increase total interest. Shorter tenure may save interest but increase monthly pressure.

Processing Fees

Processing fee is charged by some lenders for handling the loan. It may be deducted from the loan amount or added separately. Beginners must check this before finalizing.

Prepayment Rules

Prepayment means paying the loan before the scheduled end date. Some lenders may charge fees. If you expect bonus or extra income, prepayment rules become important.

Detailed Breakdown of Emergency Loans for Medical Expenses

What an Emergency Medical Loan Means

An emergency medical loan is usually a personal loan or short-term borrowing option used to manage urgent healthcare costs. It may help when savings, insurance, or family support are not enough.

The loan may be unsecured, which means no collateral is required in many cases. However, the lender may still check income, credit profile, documents, and repayment ability.

When Borrowing Makes Sense

Borrowing may make sense when the medical expense is urgent, unavoidable, and larger than available savings. It can also help when insurance reimbursement will take time but immediate payment is required.

A responsible borrower uses the loan to manage a genuine gap, not to overspend or take unnecessary debt.

When Borrowing Should Be Avoided

Borrowing should be avoided when the loan terms are unclear, interest is too high, repayment is unaffordable, or the lender seems suspicious. It should also be avoided if the same need can be managed through insurance, hospital payment plans, employer support, or savings.

Eligibility Basics

Eligibility may depend on income, employment type, credit score, existing debt, age, documents, and lender policies. Salaried people may be asked for salary slips, bank statements, identity proof, and address proof.

Interest Rate and Total Cost

The interest rate is important, but total cost is more important. A loan with a moderate interest rate and low fees may be better than a loan with a slightly lower rate but high hidden charges.

EMI and Repayment Planning

EMI planning is the heart of responsible borrowing. Before taking a loan, ask: “Can I pay this EMI every month even after rent, food, school fees, bills, and existing loans?”

Credit Score Impact

Emergency loans can affect your credit profile. Timely repayment may help maintain credit discipline. Missed payments, loan defaults, or repeated applications may create problems.

Debt Burden

Debt burden increases when a person takes multiple loans at the same time. During medical stress, avoid taking more debt than needed.

Responsible Borrowing

Responsible borrowing means taking the right amount, from a credible lender, with clear terms, and a realistic repayment plan.

Loan Comparison Basics

Compare loan amount, interest rate, tenure, EMI, processing fee, late payment fee, prepayment rule, documentation, and lender reputation.

Prepayment and Late Payment Impact

Prepayment can reduce total interest if allowed at reasonable cost. Late payment can create penalties and credit score issues. Set reminders and keep money ready before EMI date.

Mistakes to Avoid Before Applying

Do not apply everywhere at once, do not ignore terms, do not share OTPs, do not borrow extra without need, and do not take a loan from unknown sources.

Common Mistakes Beginners Make With Emergency Medical Loans

Following Random Advice

This happens when people are in panic and ask friends, social media groups, or unknown agents. It is risky because the advice may not match your income, credit profile, or repayment capacity. Instead, compare options and read terms.

Ignoring Risk

Some borrowers focus only on getting funds. They ignore EMI pressure, late fees, and credit score impact. This can create long-term financial stress. Instead, check risk before accepting money.

Not Comparing Options

Choosing the first offer may lead to higher costs. Compare at least a few suitable options before deciding.

Trusting Fake Claims

Avoid lenders or agents promising guaranteed approval, zero checks, or unrealistic benefits. Such claims may hide fraud or unfair terms.

Ignoring Hidden Charges

Processing fees, penalties, and add-ons can increase total cost. Read the agreement carefully.

Making Emotional Decisions

Medical stress can lead to rushed borrowing. Take help from a trusted family member if needed and review terms calmly.

Using Emergency Money for Risky Activities

Do not use borrowed medical funds for trading, crypto, gambling, or speculative decisions. Medical loan money should remain for medical needs.

Not Reading Terms and Conditions

Skipping terms can lead to surprise charges later. Always read before signing.

Sharing Sensitive Information

Never share OTPs, passwords, bank PINs, or sensitive documents with unknown people.

Ignoring Tax, Legal, or Compliance Responsibilities

In some cases, medical bills, insurance claims, or reimbursements may require proper records. Keep documents safely.

Depending Only on Social Media Advice

Social media can give general ideas, but it cannot replace personal financial review.

Acting in Panic or Pressure

Urgency is real, but careless borrowing can create deeper problems. Slow down enough to check basics.

Don’t Do This Checklist

- Do not borrow more than required.

- Do not accept unclear loan terms.

- Do not share OTPs or passwords.

- Do not trust guaranteed approval claims blindly.

- Do not ignore EMI affordability.

- Do not use medical loan money for risky investments.

- Do not skip reading charges and penalties.

- Do not apply through suspicious links or agents.

- Do not miss EMI dates.

- Do not hide existing debt while planning repayment.

Practical Real-Life Examples of Emergency Medical Loan Decisions

Example 1: Salaried Person Managing Month-End Medical Cost

A salaried employee faces a sudden hospital bill before salary date. The mistake would be taking a large loan without checking monthly EMI. A better action is to use available savings, check insurance, borrow only the shortfall, and select an affordable EMI. The learning is that urgent borrowing should still be planned.

Example 2: Family Handling Surgery Expenses

A family needs funds for surgery and post-care medicines. The challenge is that the hospital estimate does not include follow-up costs. A better action is to calculate treatment, medicines, tests, and recovery expenses together. The learning is that medical loan planning should include complete treatment cost, not only admission cost.

Example 3: Loan Seeker Comparing Repayment Options

A borrower sees two loan offers: one with lower EMI but longer tenure and another with higher EMI but shorter tenure. The mistake would be choosing only based on EMI. A better action is to compare total repayment cost and monthly comfort. The learning is that both EMI and total cost matter.

Example 4: Small Business Owner Facing Family Medical Emergency

A small business owner has irregular income and needs funds for a family member’s treatment. The mistake would be taking a fixed high EMI without considering seasonal income. A better action is to choose a repayment plan that matches cash flow. The learning is that repayment capacity is different for salaried and self-employed people.

Example 5: Beginner Avoiding a Fake Loan Offer

A person receives a message promising fast loan approval after paying an upfront fee. The mistake would be sharing documents and paying immediately. A better action is to verify the lender, avoid OTP sharing, and use official channels. The learning is that fraud awareness is essential during emergencies.

Two Useful Tables for Better Understanding

Table 1: Emergency Medical Funding Options Comparison

| Option | When It May Help | Key Risk | Better Approach |

|---|---|---|---|

| Emergency savings | Small or moderate medical bills | Savings may reduce quickly | Use only what is needed and rebuild later |

| Health insurance | Covered treatment expenses | Claim limits or exclusions may apply | Check coverage and documents early |

| Personal loan | Larger urgent expenses | EMI and interest burden | Compare total cost before applying |

| Employer salary advance | Short-term shortage | May reduce future salary cash flow | Use only if repayment is manageable |

| Family support | Temporary financial gap | Personal relationship pressure | Keep repayment understanding clear |

| Credit card | Small urgent payments | High cost if unpaid | Repay quickly and avoid rolling debt |

Table 2: Beginner Mistake vs Correct Emergency Loan Approach

| Beginner Mistake | Why It Is Risky | Correct Approach |

|---|---|---|

| Borrowing in panic | May lead to high-cost debt | Pause and compare basic terms |

| Ignoring EMI capacity | Can cause missed payments | Check monthly budget first |

| Not reading charges | Total cost may increase | Review fees and penalties |

| Applying everywhere | May affect credit profile | Apply selectively |

| Trusting unknown agents | Fraud risk increases | Use verified lenders only |

| Borrowing extra money | Creates unnecessary debt | Borrow only the real shortfall |

Tools, Methods, and Frameworks Readers Can Use

EMI Calculator

An EMI calculator helps estimate monthly repayment before taking a loan. Beginners can enter loan amount, interest rate, and tenure to understand affordability. It helps avoid the mistake of choosing a loan that looks manageable but becomes stressful later.

Medical Expense Sheet

A simple expense sheet helps list hospital charges, medicines, diagnostic tests, travel, attendant costs, and follow-up treatment. It prevents underestimating the total amount needed.

Loan Comparison Checklist

A loan comparison checklist helps compare interest rate, tenure, EMI, processing fee, late fee, prepayment rules, and lender credibility. It helps avoid choosing a loan only because it is easily available.

Credit Score Review

Checking credit score awareness helps borrowers understand their borrowing position. It also reduces the chance of applying randomly to many lenders without planning.

Debt-to-Income Review Method

This method compares total monthly EMIs with income. It helps identify whether another EMI is safe. Beginners should use this before accepting a new loan.

Emergency Budget Reset

After taking a medical loan, review monthly expenses and reduce non-essential spending for a few months. This helps manage EMI without disturbing essential family needs.

Document Folder Method

Keep hospital bills, prescriptions, insurance documents, loan agreement, EMI schedule, and payment receipts in one folder. This helps with claims, records, and future reference.

Expert Tips to Make Better Decisions

1. Borrow Only the Required Amount

This matters because extra borrowing increases EMI and interest. Apply it by calculating the actual shortfall after checking savings and insurance.

2. Compare Total Loan Cost, Not Only EMI

A low EMI may come with a long tenure and higher total interest. Compare processing fee, tenure, and total repayment before deciding.

3. Keep Medical Bills and Records Safe

Medical documents may be needed for insurance claims, reimbursements, or future review. Store bills, prescriptions, and discharge summaries properly.

4. Avoid Unverified Loan Agents

Fraud risk increases during emergencies. Use official lender channels and never share OTPs, passwords, or bank PINs.

5. Check EMI Comfort Before Approval Amount

Getting approved for a higher amount does not mean you should borrow it. Choose an EMI that fits your monthly income safely.

6. Avoid Multiple Loan Applications

Applying everywhere may create confusion and may affect your credit profile. Shortlist suitable options and apply carefully.

7. Read Prepayment Rules

If you expect a bonus or reimbursement, prepayment may help reduce debt. But first check whether charges apply.

8. Do Not Use Medical Loan Money for Risky Activities

Medical funds should be used for treatment needs only. Avoid using borrowed money for trading, crypto, gambling, or speculative activities.

9. Create an EMI Reminder System

Missed EMIs can lead to penalties and credit issues. Set calendar reminders or auto-debit only when you are sure funds will be available.

10. Rebuild Emergency Savings After Repayment Starts

Once the situation stabilizes, start rebuilding savings slowly. Even a small monthly amount can help reduce future borrowing.

11. Take Professional Advice When Needed

If the loan amount is large, repayment is complex, or medical insurance is involved, consult a qualified professional. Good advice can prevent costly mistakes.

12. Review Household Expenses Temporarily

During repayment, reduce non-essential spending. This may include subscriptions, luxury purchases, or avoidable lifestyle expenses.

13. Keep Family Communication Clear

Medical loans affect the household budget. Discuss repayment plans with family members to avoid confusion and pressure.

14. Avoid Guaranteed Approval Claims

No genuine loan should be accepted only because someone claims guaranteed approval. Always check terms, lender identity, and repayment cost.

15. Think Beyond the Emergency

The emergency may end, but repayment continues. Make decisions that protect future financial stability.

Case Studies: How Better Understanding Changes Decisions

Case Study 1: Salaried Employee With Limited Savings

Profile:

Rohit is a salaried employee with regular income and limited emergency savings.

Situation:

His father needs urgent medical tests and short hospital admission.

Problem:

The total cost is higher than his available savings.

Wrong approach:

He almost accepts the first loan offer without checking processing fee and EMI.

Better approach:

He checks insurance support, uses part of savings, compares two loan options, and borrows only the remaining amount.

Result or learning:

His EMI stays manageable, and he avoids unnecessary extra borrowing.

Key takeaway:

Even in emergencies, borrowing should be based on need, not panic.

Case Study 2: Self-Employed Person With Irregular Income

Profile:

Meena runs a small business and her income changes month to month.

Situation:

A family member needs treatment, and she needs funds immediately.

Problem:

A fixed high EMI could disturb her business cash flow.

Wrong approach:

She considers taking a short-tenure loan with high EMI.

Better approach:

She chooses a repayment plan after reviewing average monthly income, business expenses, and family needs.

Result or learning:

She avoids overcommitting and keeps both treatment and business expenses under control.

Key takeaway:

Self-employed borrowers must match EMI planning with realistic cash flow.

Case Study 3: Beginner Avoiding Loan Fraud

Profile:

Amit is a first-time borrower searching for urgent medical funds online.

Situation:

He receives messages from unknown lenders promising easy approval.

Problem:

One agent asks for an upfront fee and OTP.

Wrong approach:

He nearly shares sensitive details because he needs money urgently.

Better approach:

He stops, verifies the source, avoids sharing OTP, and chooses a trusted channel.

Result or learning:

He protects his personal data and avoids possible fraud.

Key takeaway:

Urgency should not remove basic safety checks.

Risk Awareness: What Readers Must Check First

Credit Risk

Credit risk means the possibility of damaging your credit profile through missed payments or default. It matters because future loans may become difficult or expensive. Reduce this risk by choosing affordable EMIs and paying on time.

Interest Rate Risk

Interest rate risk means paying more than expected because of high borrowing cost. Reduce it by comparing lenders and checking total repayment.

Over-Borrowing Risk

Over-borrowing means taking more money than needed. It increases EMI pressure. Reduce it by calculating the real medical shortfall.

Fraud Risk

Fraud risk is high when borrowers are desperate. Fake agents may ask for upfront fees, OTPs, or personal documents. Reduce it by using verified platforms and never sharing sensitive access details.

Data Privacy Risk

Loan applications require personal and financial documents. Reduce this risk by sharing documents only through secure and trusted channels.

Liquidity Risk

Liquidity risk means not having enough money left for daily needs after paying EMI. Reduce it by keeping a monthly cash buffer.

Emotional Risk

Medical emergencies can lead to panic decisions. Reduce emotional risk by involving a trusted family member and using a checklist.

Legal and Compliance Risk

Loan agreements are legal commitments. Reduce risk by reading terms and asking questions before signing.

Misinformation Risk

Online advice may be incomplete or misleading. Reduce it by verifying details and consulting qualified professionals where required.

Checklist Before Taking Action

- I understand the actual medical expense clearly.

- I have checked savings, insurance, and employer support first.

- I have calculated the exact borrowing gap.

- I have compared interest rate, EMI, tenure, and processing fee.

- I have checked repayment capacity.

- I have reviewed hidden charges and late payment penalties.

- I have read prepayment and foreclosure rules.

- I have avoided fake approval or unrealistic loan claims.

- I have protected my personal data, OTP, and banking details.

- I have kept medical bills and loan documents safely.

- I have prepared a written repayment plan.

- I have avoided emotional borrowing.

- I have considered professional advice if the amount is large.

- I have planned how to rebuild emergency savings later.

Use this checklist before applying for a loan, not after accepting one. It helps you slow down, compare properly, and avoid decisions that can create long-term debt stress.

Strategic Insights for Better Loan Decisions

Debt-to-Income Ratio

This compares your monthly debt payments with monthly income. Beginners can use it to understand whether another EMI is safe. If EMIs already consume too much income, taking a new loan may create pressure.

EMI Burden

EMI burden is the pressure created by monthly repayment. A smaller EMI may feel comfortable, but always check total interest. A balanced EMI is better than choosing the lowest EMI blindly.

Credit Score Management

A medical loan should not damage your credit health. Pay on time, avoid unnecessary applications, and keep repayment records.

Prepayment Planning

If you expect reimbursement, bonus, or extra income, check whether partial prepayment is allowed. This can help reduce outstanding debt if charges are reasonable.

Loan Restructuring Awareness

If repayment becomes difficult, speak to the lender early instead of ignoring EMIs. Delayed communication may increase penalties and stress.

Short-Term vs Long-Term Debt Impact

Short-term loans may have higher EMI but close faster. Long-term loans may reduce EMI but increase total repayment. Choose based on income stability and total cost.

Emergency Fund Planning

After the medical situation stabilizes, start rebuilding an emergency fund. This reduces dependency on loans for future urgent needs.

Insurance Review

Medical emergencies show the importance of health insurance awareness. Review coverage, exclusions, claim process, and family medical needs regularly.

Key Terms Explained for Beginners

- Emergency Loan: A loan used to manage urgent expenses such as medical bills, repairs, or sudden family needs. It must be repaid with interest and charges.

- Medical Loan: A borrowing option used specifically for healthcare-related expenses such as treatment, surgery, medicines, or hospital bills.

- Interest Rate: The cost of borrowing money. A higher interest rate increases total repayment.

- EMI: EMI means Equated Monthly Instalment. It is the fixed amount paid every month to repay the loan.

- Loan Tenure: The time period given to repay the loan. Longer tenure may reduce EMI but can increase total interest.

- Processing Fee: A fee charged by some lenders for processing the loan application.

- Credit Score: A number that reflects your credit behaviour. Timely repayment can support credit health, while missed payments can harm it.

- Prepayment: Paying part or full loan amount before the scheduled end date. Some lenders may charge for it.

- Late Payment Fee: A penalty charged when EMI is not paid on time.

- Debt Burden: The pressure created by existing loans and EMIs on monthly income.

- Repayment Capacity: Your ability to repay a loan comfortably after managing regular expenses.

- Hidden Charges: Extra costs that may not be obvious at first, such as bounce charges, service fees, or insurance add-ons.

- Loan Agreement: A legal document that explains loan terms, charges, repayment rules, and borrower responsibilities.

- Cashless Insurance Claim: A facility where the insurer directly settles eligible hospital bills with the hospital, subject to policy terms.

- Reimbursement Claim: A claim where you pay first and later submit documents to the insurer for eligible repayment.

Who Should Read This Blog

Beginners

Beginners can understand how emergency loans work without complicated finance language.

Students

Students can learn basic money management and medical emergency planning for family awareness.

Salaried Employees

Salaried people can learn how to manage sudden expenses before salary without damaging monthly budgets.

Small Business Owners

Business owners can understand how irregular income affects EMI planning.

New Investors

New investors can learn why emergency money should not be used for risky investments.

Traders

Traders can understand why borrowed medical funds should never be used for speculative trading.

Loan Seekers

Loan seekers can learn how to compare loans, check charges, and avoid debt traps.

Crypto Learners

Crypto learners can understand why emergency borrowed money should not be used in volatile assets.

Casino Content Creators

Casino content creators can learn responsible financial language and avoid misleading borrowing or money claims.

Finance Bloggers

Finance bloggers can use this topic to explain responsible borrowing, risk awareness, and beginner money planning.

People Improving Money Awareness

Anyone trying to avoid financial mistakes can learn practical steps for emergency planning.

Frequently Asked Questions

1. What is an emergency loan for medical expenses?

An emergency loan for medical expenses is money borrowed to manage urgent healthcare costs. It may cover hospital bills, tests, medicines, surgery, or recovery expenses. Borrowers should check EMI, interest, charges, and repayment capacity before applying.

2. Why is How to Manage Sudden Medical Expenses With Emergency Loans important?

How to Manage Sudden Medical Expenses With Emergency Loans is important because medical emergencies can create panic. A clear plan helps borrowers avoid high-cost debt, hidden charges, and repayment stress while arranging funds responsibly.

3. Should I use savings before taking a medical loan?

Yes, check savings, insurance, and employer support before borrowing. A loan should usually cover the remaining gap, not the full amount if other safe options are available.

4. What is the biggest mistake beginners make with emergency loans?

The biggest mistake is borrowing in panic without checking EMI, interest rate, fees, and repayment ability. This can create long-term financial pressure after the medical emergency is over.

5. How can I compare emergency loan options?

Compare interest rate, EMI, tenure, processing fee, late payment charges, prepayment rules, and lender credibility. Do not choose only based on fast approval or low EMI.

6. Is an emergency medical loan useful for salaried people?

It can be useful if the expense is urgent and salary or savings are not enough. Salaried people should ensure the EMI fits their monthly budget after rent, bills, food, and existing loans.

7. Can emergency loans affect my credit score?

Yes, repayment behaviour can affect your credit profile. Timely payments may support credit discipline, while missed EMIs or defaults may create future borrowing problems.

8. What should I avoid before applying for an emergency loan?

Avoid unknown agents, upfront fee demands, OTP sharing, unclear terms, unnecessary borrowing, and multiple random applications. Always verify the lender and read the loan agreement.

9. How to Manage Sudden Medical Expenses With Emergency Loans safely?

To manage sudden medical expenses safely, calculate the actual need, check insurance, compare loan options, choose affordable EMI, read terms, and protect personal data. Borrow only what is necessary.

10. Should I take professional advice before borrowing?

If the loan amount is large, terms are confusing, or insurance and legal documents are involved, professional advice can help. A qualified financial or legal expert can guide better decisions.

11. Can I repay an emergency loan early?

Some lenders allow prepayment, but rules and charges may vary. Check prepayment terms before taking the loan, especially if you expect reimbursement or bonus income.

12. What is the best next step after reading this blog?

The best next step is to prepare a personal emergency plan. Review savings, health insurance, monthly budget, borrowing capacity, and important documents before a real emergency happens.

Conclusion and Next Steps

Managing sudden medical expenses requires both emotional strength and financial clarity. An emergency loan can be helpful when treatment is urgent and savings or insurance are not enough, but it must be used responsibly. Beginners should remember that loan approval is not the final goal; safe repayment is equally important. Before borrowing, calculate the actual medical need, check insurance support, compare loan options, read terms carefully, and choose an EMI that fits your monthly budget. Avoid panic decisions, fake approval claims, hidden charges, and unnecessary borrowing. After the emergency is handled, review your repayment plan and start rebuilding your emergency fund slowly. The most important lesson is simple: medical emergencies may be sudden, but your financial decisions should still be calm, informed, and practical. With the right approach, you can manage urgent healthcare costs while protecting your future financial stability.