Introduction

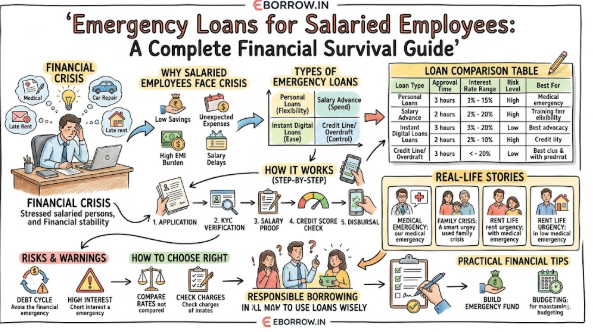

Financial stability is often planned, but emergencies are not. As a working professional, you may manage your monthly budget with precision, yet an unexpected medical bill, a sudden car repair, or a delay in salary can disrupt your plans instantly. When the gap between your needs and your available funds widens, emergency loans for salaried employees provide a necessary bridge to maintain your financial health.

This guide explores how these financial tools work, the risks involved, and how to use them responsibly to navigate a difficult period.

What are Emergency Loans for Salaried Employees?

An emergency loan is a short-term financial product designed to provide rapid access to liquidity. Unlike long-term loans for homes or education, these are specifically tailored to meet immediate needs.

For salaried individuals, these loans often leverage your steady income as a primary form of security. They are built for speed, transparency, and accessibility, helping you cover urgent costs without the lengthy wait times associated with traditional bank products.

Why Salaried Employees Face Cash Crisis Situations

Even with a steady paycheck, many professionals experience periods of financial stress. Understanding the root causes is the first step toward better management:

- Unexpected Expenses: Sudden medical emergencies or urgent home repairs can cost more than your current month’s savings.

- High EMI Burdens: If a large portion of your monthly income goes toward existing debts, there is little room for maneuver when a new cost arises.

- Salary Delays: Administrative or company-related issues that delay your paycheck can leave you unable to pay rent or utility bills on time.

- Lifestyle Inflation: Increasing spending along with salary increases can leave you with thin financial margins.

Types of Emergency Loans

When you are looking for an instant personal loan for salary employees, you have several options:

- Personal Loans: These are versatile and can be used for any purpose. They usually offer larger amounts but require a bit more documentation.

- Salary Advance Loans: Some employers or specialized digital lenders offer advances against your next month’s salary, which is a common way to get an emergency cash loan.

- Instant Digital Loans: These are app-based solutions that offer quick approval personal loans by evaluating your digital footprint and bank statement.

- Credit Line / Overdraft Facility: This acts as a revolving credit limit, allowing you to borrow only what you need and pay interest only on the amount used.

How Emergency Loans Work: The Process

Understanding the workflow helps reduce the stress of the application process.

- Application: You submit an online form with basic personal and employment details.

- KYC Verification: You provide identity and address proof digitally.

- Salary Proof Check: Lenders verify your monthly income via salary slips or bank statements.

- Credit Evaluation: Your credit score is checked to assess repayment capacity.

- Approval & Disbursal: Once approved, funds are transferred to your bank account, often within hours.

Eligibility and Requirements

To ensure a smooth application for emergency loans for salaried employees, keep these criteria in mind:

- Employment: You must be a permanent employee at a registered company.

- Salary: A minimum monthly income threshold is usually required.

- Credit Score: A healthy score indicates reliability and helps in securing better rates.

- Documents: You will typically need your PAN card, official identity documents, recent salary slips, and the last 3–6 months of bank statements.

Comparison of Emergency Loan Options

| Loan Type | Approval Time | Interest Rate Range | Risk Level | Best For |

| Personal Loan | 24–48 Hours | Moderate | Low | Medium Expenses |

| Salary Advance | Instant | Moderate | Low | Short-term Gap |

| Credit Card Cash | Instant | High | High | Extreme Urgency |

| Instant App Loans | < 2 Hours | High | Medium | Very Small Needs |

| Bank Overdraft | 1–2 Days | Moderate | Low | Flexibility |

Real-Life Stories

1. The Medical Emergency

Rohan needed urgent funds for a family member’s hospital admission. He opted for an instant personal loan. Because he had his documents ready, the money was disbursed within four hours, allowing the surgery to proceed without delay.

2. The Salary Delay

Priya faced a delay in her company payroll just as her rent was due. She took a small salary advance loan. She repaid it as soon as her salary arrived, avoiding late fees from her landlord.

3. The Family Crisis

Anita faced an unexpected travel expense due to a family emergency. She used a bank overdraft facility, which gave her the flexibility to borrow only what she needed.

4. Rent Payment Urgency

Vikram, a young professional, found his bank account drained due to a vehicle repair. An instant digital loan helped him cover his rent. He learned the value of keeping a small buffer in his savings account.

5. Credit Card Limit Exhaustion

Sunita had her credit card blocked due to a technical error during travel. A short-term personal loan provided the cash she needed to get home safely.

Benefits and Risks

Benefits:

- Quick Relief: Immediate access to funds when time is a factor.

- No Collateral: Most of these loans are unsecured, meaning you don’t need to pledge assets.

- Easy Online Application: Most processes are digital and require minimal paperwork.

Risks:

- Interest Costs: Quick loans often come with higher interest rates than traditional loans.

- Debt Cycles: If you borrow without a repayment plan, you risk falling into a cycle of debt.

- Credit Impact: Missing even one repayment can significantly damage your credit score.

Practical Financial Tips

To avoid relying on emergency loans for salaried employees, aim to:

- Build an Emergency Fund: Save 3–6 months of expenses in a liquid account.

- Salary Planning: Budget your expenses on the day the salary arrives.

- Track Spending: Use simple apps to monitor where your money goes each month.

Frequently Asked Questions

- What are emergency loans for salaried employees?

These are short-term financial products designed to cover sudden, urgent expenses. They allow you to bridge a temporary gap in cash flow using your steady monthly income as a base. - How quickly can I get an emergency loan?

Depending on the lender and your digital readiness, many instant loans can be approved and disbursed within a few hours to 24 hours. - What is the minimum salary required?

Each lender sets its own criteria, but most require a stable, verifiable monthly income that demonstrates you have the capacity to repay the loan on time. - Can I get a loan without a credit score?

While some lenders may offer smaller amounts, most traditional and reliable digital lenders require a credit score to assess your risk profile and offer reasonable interest rates. - Are emergency loans safe?

If you choose a reputable, RBI-registered lender, they are safe. Always verify the lender’s credentials on their official website before sharing any documents. - What is the interest rate for instant loans?

Interest rates for instant loans are generally higher than standard personal loans due to the speed and convenience they offer. Always check the annual percentage rate (APR). - Can I get a loan during a salary delay?

Yes, many salaried employees use short-term advances or personal loans to manage expenses during temporary salary delays. Ensure you have a clear plan to repay when the salary arrives. - What documents are required?

You will typically need proof of identity (such as your PAN Card), address proof, recent salary slips, and bank statements showing regular salary credits. - Does a loan affect my credit score?

Yes. Your repayment behavior—whether you pay on time or miss a payment—will be reported to credit bureaus and will impact your score. - What happens if I miss a repayment?

Missing a repayment can lead to late fees, collection calls, and a significant drop in your credit score, which may make it harder to get loans in the future.

Conclusion

Emergency loans serve as a powerful safety net, but they should never be viewed as a permanent solution to persistent financial strain. While they provide immediate relief during a financial crisis, the real strength of a salaried employee lies in proactive planning.

Building an emergency buffer, maintaining a disciplined budget, and understanding your debt-to-income ratio are essential habits that reduce the need for high-interest borrowing. Before you sign any loan agreement, ensure that the repayment schedule aligns perfectly with your future cash inflows. Use these financial tools as a strategic necessity rather than a crutch.